CARY, NC — February 1, 2024 — INDA, the Association of the Nonwoven Fabrics Industry, announced that exhibit space reservations for IDEA®25 are rapidly approaching 70 percent capacity. INDA encourages all potential exhibitors to make their reservations as soon as possible to ensure they receive the best location for their booth. IDEA is being held April 29-May 1, 2025 at the Miami Beach Convention Center in Miami Beach, Florida.

Global suppliers and manufacturers who exhibit at IDEA will connect their technologies and innovations to C-suite leaders, R&D developers, and specifiers. Exhibitors can demonstrate their products to participants from around the world, answer their technical questions, and collaborate on new products.

INDA is responding to customer feedback with reduced expo pass fees for attendees and exhibitors to drive additional networking and business development opportunities. FiltXPO™, the International Filtration Conference & Exhibition, will again be co-located with IDEA bringing additional value to all participants. Registrants can attend both shows whether they are attending the expo or the conference and expo.

Tony Fragnito, INDA President, said, “Our theme for IDEA25 is ‘Nonwovens for a Healthier Planet’ and will culminate our 2024 focus on Sustainability with pillars on Responsible Sourcing, End-of-life Solutions and Innovations in Sustainability. We are excited to see the diversity of companies showcasing their commitment to sustainable concepts. This event is where the future of nonwovens will be on display.”

“Exhibit space for IDEA is being reserved at a brisk pace, with interest from both prior exhibitors as well as companies exhibiting for the first time. This show is where nonwoven companies can cement their status as a solution provider, acquire competitive market intelligence, and grow their business with new market applications,” said Joe Tessari, INDA Associate Director of Sales.

IDEA is the largest North American exhibition dedicated to the next generation of nonwovens and engineered materials. To learn more about exhibiting at IDEA, visit www.ideashow.org.

Posted: February 1, 2024

Source: INDA, the Association of the Nonwoven Fabrics Industry,

In the rapidly evolving landscape of retail, the e-commerce market has emerged as a dominant force, transforming the way consumers shop for goods, including textiles. As online shopping continues to gain momentum, the textile industry is faced with the challenge of adapting its supply chain solutions to meet the unique demands of the digital marketplace.

The traditional textile supply chain, characterized by a linear flow from raw material production to manufacturing, distribution, and finally, retail, is now being reshaped to accommodate the dynamic nature of e-commerce. Here, we explore the key strategies and technologies that are revolutionizing textiles supply chain solutions for the e-commerce market.

Demand Forecasting And Data Analytics

In the e-commerce era, accurate demand forecasting is crucial for efficient inventory management. Data analytics plays a pivotal role in analyzing consumer behavior, predicting trends, and optimizing production schedules. Textile companies are increasingly leveraging advanced analytics tools to gain insights into market trends, enabling them to align production with actual demand, reduce excess inventory, and minimize the risk of stockouts.

Agile Manufacturing

Traditional manufacturing processes often involve large production runs to achieve economies of scale. However, the unpredictable nature of e-commerce demand calls for more agile manufacturing practices. Textile companies are adopting flexible production systems that can quickly adjust to changes in demand, allowing for smaller, more frequent production runs. This not only reduces the risk of overproduction but also enables companies to respond rapidly to market trends.

Eco-Friendly Practices And Sustainability

As consumers become more environmentally conscious, there is a growing demand for sustainable and eco-friendly products. Textile companies are integrating sustainable practices into their supply chains, from sourcing raw materials to manufacturing and distribution. E-commerce platforms are also recognizing the value of eco-friendly products, and textiles with sustainability credentials are gaining a competitive edge in the market.

Digitization Of Processes

The digitization of supply chain processes is a cornerstone of adapting to the e-commerce market. From order placement to production and delivery, digital technologies streamline operations, reduce lead times, and enhance overall efficiency. The implementation of digital platforms for order processing, inventory management, and communication between stakeholders ensures real-time visibility and collaboration throughout the supply chain.

Fulfillment And Logistics Optimization

E-commerce success hinges on timely and efficient order fulfillment. Textile companies are investing in advanced warehouse management systems, automated picking and packing technologies, and last-mile delivery solutions to enhance the speed and accuracy of order processing. Additionally, partnerships with third-party logistics providers are becoming increasingly popular, allowing textile companies to tap into existing delivery networks and meet the demands of quick and reliable shipping.

Customer-Centric Approach

In the e-commerce landscape, customer satisfaction is paramount. Textile companies are adopting a customer-centric approach by offering personalized experiences, customization options, and transparent communication throughout the purchasing process. Leveraging technology, such as virtual fitting rooms and augmented reality, enables customers to make more informed decisions, reducing the likelihood of returns and improving overall customer satisfaction.

Adaptive Technology Integration

The integration of cutting-edge technologies, such as blockchain for supply chain transparency and artificial intelligence for predictive analytics, is becoming a norm in the textiles industry. These technologies enhance traceability, minimize counterfeiting risks, and improve overall supply chain visibility, ensuring that products reach consumers with the highest level of quality and authenticity.

Summing Up

The e-commerce revolution is reshaping the textiles supply chain, necessitating a shift from traditional linear models to more adaptive and agile approaches. By embracing demand forecasting, agile manufacturing, sustainability practices, digitization, logistics optimization, customer-centric strategies, and advanced technology integration, the textile industry is poised to thrive in the digital era. As e-commerce continues to evolve, textile companies must remain proactive in adopting innovative solutions to meet the ever-changing demands of online consumers and stay competitive in the global marketplace.

Editor’s Note: Rohit Dev Sethi is managing director of India-based Colossustex Pvt. Ltd.

ITMA 2023 was held at the Fiera Milano Rho fairgrounds in Milan, Italy.

TW Special Report

ITMA 2023 is now in the textile industry’s rear-view mirror, but for exhibiting companies leads, connections and information accumulated during the event are starting points for future business opportunities and ideas for the next generation of technologies.

Textile World recently interviewed just a very small sample of exhibitors that participated in ITMA 2019, held in Milan, Italy, to learn about their experience and get a sense of the overall market for textile investment especially as it relates to the United States.

Responses below were provided by Will Motchar, Navis TubeTex; Hardy Sullivan, Thies Corp.; Rick Stanford, Baldwin Technology Co. Inc.; Gunar Meyer, Monforts; Stefan Engel, American Trützschler; and Thomas Oetterli, Rieter Group.

Responses are in no particular order and have been condensed and edited for clarity.

Respondent: Will Motchar, president and CEO of Navis TubeTex, Lexington, N.C.

TW: Can you comment on the quantity and quality of visitors at your booth during the show, and the countries and regions where the visitors came from? Motchar: Quantity and quality of visitors was excellent at ITMA. As always, ITMA is a truly global show so we had current and potential customers from around the world. I would say South Asia was very strong, central and south America, and even the U.S. was well represented.

TW:Of the machines/technology your company had on display, what drew the most attention? Motchar: Our newest acquisition, Gaston Systems foaming technology drew the most attention for us. The technology has been traditionally used for chemical application offering significant benefits in terms of reduced chemical, water, and energy usage. We now have the capability to use the Gaston technology to dye fabrics and even yarn in a continuous process that is far more sustainable than current methods.

TW: Based on customers’ interests and questions during the show, do you see any overarching trends? In your sector, what impact does sustainability have? Motchar: Well you said it, sustainability is the overarching trend. But customers want and HAVE to have real sustainable solutions, not just hyperbole. Too many suppliers are slapping the word “sustainability” on their newest models when the improvements are miniscule to non-existent.

TW: What is the appetite for investing? Is U.S. interest apparent? Motchar: Discussions at ITMA were very positive for investment. However, we have not seen actual orders come in as fast as we anticipated following the exhibition. Interest from U.S. customers was very high, but they also have delayed ordering.

TW: Do recent orders point to any evidence of nearshoring and reshoring in the Western Hemisphere? Motchar: Yes, definitely. There is no denying that we are seeing this happen. Probably a higher degree of nearshoring than reshoring, but both are happening.

TW: Do inflation and higher interest rates create investment headaches? Do you think the United States will avoid a recession? Motchar: Absolutely. Inflation and high interest rates are a problem. Inflation is killing the lower and middle class buying power. Interest rates obviously play a big role in capital investment decisions. I do not think the U.S. will avoid a recession.

TW: Are there any roadblocks, such as high energy prices, holding manufacturers back from investing in new equipment and technologies? Motchar: If anything, high energy prices are driving manufacturers to invest in new equipment and technologies that use less energy. The biggest roadblock for investing is uncertainty. Geopolitical and economic conditions are very volatile and unpredictable. That is a bad recipe for investment.

TW: Would you say ITMA 2023 was an overall success for your company? Motchar: If we see the orders come in that were anticipated following the show it will be an overall success. Nevertheless it was a great opportunity to showcase all the new and exciting products/technologies that we have been working on.

Respondent: Hardy Sullivan, sales, Thies Corp., Rock Hill, S.C.

TW: Can you comment on the quantity and quality of visitors at your booth during the show, and the countries and regions where the visitors came from? Sullivan:We were pleased with the traffic in terms of quantity of visitors from the Americas, Europe and India. The lingering effects of Covid probably resulted in a smaller turnout from China. While there weren’t a lot of deals negotiated on-site, some ITMA visits turned into sales. In other cases, however, promising projects have been delayed. Being at ITMA was the right decision but the results have been mixed.

TW: Of the machines/technology your company had on display, what drew the most attention? Sullivan: Practically every discussion started with Signature Series because of its strong environmental story and low operational cost. It was, literally, the centerpiece of our booth. Being able to prepare and dye cotton without salt in a dye jet is a compelling advancement. Of course, each customer has his own area of interest, so our focus follows the individual need.

TW: Based on customers’ interests and questions during the show, do you see any overarching trends? In your sector, what impact does sustainability have? Sullivan: For sure, sustainability and digitalization, which is a subset of sustainability, were the overarching trends. Sustainability was our booth’s theme but, more importantly, it has been our engineering mission. To set our story apart, we openly reported metrics that quantify usages of water, materials, and electricity; and we benchmark our values to the next-best offering, not outdated standards.

TW: What is the appetite for investing? Is U.S. interest apparent? Sullivan: U.S. textile producers tend to evolve capabilities rather than make greenfield, step-change investments in technology or new products.

In the United States there are relatively small but important pockets of customer interest. A few examples of domestically-dyed end-uses include automotive fabrics, military fabrics, and upholstery yarns. Fiber cleaning and bleaching for nonwoven products, such as facial wipes, is another important market for us.

As happens in textiles, in the ‘90s and ‘00s there was an exodus of large-scale apparel dyers from the US to lower-cost countries. While the US is not a strong market for dye machines, relatively, Thies US is well-prepared to support dyers that remain committed to domestic production. Large orders are infrequent, so we’re building machines for niche manufacturers and customizing automated chemical management solutions. The latter systems offer safe, hands-free blending and dispensing of fabric finishes and coatings to fabric applicators (i.e. pads, spray systems).

Thies produces machines in Germany but the technical, commercial, and warehousing support is local.

TW: Do recent orders point to any evidence of nearshoring and reshoring in the Western Hemisphere? Sullivan: Unfortunately, the evidence is not overwhelming. We have had some pleasant surprises from orders from Mexico. However, some near-shoring decisions appeared to have slowed. With their economy struggling, are Chinese mills lowering prices to overcome slow supply and high transportation costs that were experienced during Covid? We’re not sure.

TW: Do inflation and higher interest rates create investment headaches? Do you think the United States will avoid a recession? Sullivan: US consumers have an oversized appetite for taking on debt, as evidenced by credit card debt reaching pre-pandemic levels. Inevitably, however, paying more for housing, in particular, is going to cut into consumer demand, particularly for semi-durable and durable goods. In turn, our customer base may see a slowdown in sales.

A recent WSJ article indicated the US economy, which has been resilient, might have a soft landing, meaning lower inflation without a recession. I think a recession will be narrowly avoided … but our long-term problem, which is not being addressed, is rising debt.

TW: Are there any roadblocks, such as high energy prices, holding manufacturers back from investing in new equipment and technologies? Sullivan: On the contrary, the US still has relatively low energy prices. When natural gas prices were high — early 2022 (Russia invaded Ukraine) — there was a spike in interest in our technologies that consume less fuel and recover energy from heated effluent. Now that the fuel price pressure has subsided, paybacks are longer and interest has softened a bit.

Of course, higher energy consumption has another cost — higher emissions of greenhouse gases. For now, at least, this environmental cost does not show up in ROI calculations. As a result, this aspect of sustainability is not the driving factor for capital decisions.

TW: What are your thoughts on the impact of artificial intelligence (AI) in textile manufacturing and the technology your company designs/supplies? Sullivan: I wouldn’t say we’re using AI today, meaning systems are working to make improvements without human intervention. However, we do have customers that are taking full advantage of tools to work smarter.

Smart systems in use today consist of (1) an understanding of materials and processes (by smart, informed people), (2) user-friendly software networked to advanced machines for controlling process settings, (3) automatic, real-time measurement of process variables, (4) maintenance of wear-and-tear components, and (5) continuous implementation of lessons learned.

As a technical example, we offer chemical dispensing systems that have a self-learning feature. A pump dispenses a predetermined volume and that volume is then measured by a flow meter. If the flow meter indicates more or less chemical than expected, then the pump will adjust its number of revolutions, accordingly, during the next dispense. In another example, we can easily ensure certain chemicals do not get combined in future recipes if we identify a negative interaction. Lastly, I can envision a central system that shortens time spent problem-solving by analyzing data trends in an automated way. For me, having a system that implements decisions without human intervention (AI) is a step too far, at least for now.

I think the most important job we have at Thies is to educate customers on the potential that already exists.

Rick Stanford, VP global business development at Baldwin

Respondent: Rick Stanford, vice president of Global Business Development, Textiles, Baldwin Technology Corp., St. Louis

TW: Can you comment on the quantity and quality of visitors at your booth during the show, and the countries and regions where the visitors came from? Stanford: We had more than 300 visits with the vast majority high quality contacts. As you can imagine a concentration of visitors came from Pakistan, Bangladesh, India, Turkey, Western Europe. We heard that some Indians were not able to get their visas so traffic from India could have been better. We saw good traffic from Taiwan and Japan. I would say the Americas is about what you would expect. Not so many visitors, but very serious opportunities.

TW: Based on customers’ interests and questions during the show, do you see any overarching trends? In your sector, what impact does sustainability have? Stanford: In dyeing and finishing, sustainability and lowering the carbon footprint is the most important. Our technology’s main objectives are in these areas. We believe that this ITMA was sustainability front and center and then mills were focused on how to improve their processes more than purchasing more production capacity. During COVID there was a big push for more production as people were working from home and looking for more comfortable, casual clothes. Now the mills have the capacity and want to be more sustainable with a lower carbon footprint.

TW: What is the appetite for investing? Is U.S. interest apparent? Stanford: Asia is looking to invest. We actually sold machines at the show. For our technology, the U.S. is interested, but quite honestly, because of the poor business conditions, the U.S. mills are holding off on investment. It really has not improved since the show.

TW: Would you say ITMA 2023 was an overall success for your company? Stanford: Overall, it was the best ITMA I attended. I have attended each ITMA since Hanover in 1991. Baldwin has the products that the market is looking for and that helps. It was a well organized very successful exhibition. Many times exhibitions are a bit disappointing when you consider the money and people resources that are required. With this show, it definitely paid dividends!

Stefan Engel

Respondent: Stefan Engel, CEO, Trützschler USA, Charlotte, N.C.

TW: Can you comment on the quantity and quality of visitors at your booth during the show, and the countries and regions where the visitors came from? Engel: We were very pleased with the quantity and quality of our discussions. The fact that the total number of visitors at this ITMA was higher than at the ITMA 2019 was also reflected at our stand. We had a very good response at our booth and recorded more than 1200 “qualified” conversations with visitors from all over the world.

TW: Of the machines/technology your company had on display, what drew the most attention? Engel: Trützschler Spinning experienced a strong demand for its recycling solutions and the new cooperation with the Turkish company Balkan Textile Machinery INC.CO. This has made us the first full liner in the spinning preparation and recycling sector, as our product portfolio is now completed by Balkan’s cutting and tearing machines. Further, the next generation card TC 30i attracted a lot of attention. It achieves the best quality from any raw material thanks to an enlarged cylinder diameter and a higher number of active flats. Another highlight was our 12-head high-performance comber TCO 21XL that maximizes productivity by 50 % without sacrificing quality – while saving 25 % space. A special topic for Trützschler Nonwovens was the presentation of customized needle-punching solutions together with the Italian company Texnology S.l.r.

TW: Based on customers’ interests and questions during the show, do you see any overarching trends? In your sector, what impact does sustainability have? Engel: Sustainability continues to be one of the biggest trends and it has a big impact. Our customers are always looking for cost-effective solutions to make our industry more sustainable. As a fabric manufacturer you have a lot of textile waste. You can use this waste as a raw material to make new yarn, for example. In general, using textile waste as a raw material can be an attractive business model if you can achieve a certain level of quality. Our spinning preparation machines achieve this level.

TW: What is the appetite for investing? Is U.S. interest apparent? Engel: Most investments of our U.S. customer base increased between late 2020 and topped mid-2022. As delivery times increased dramatically over the same period due to supply chain issues, some customers began to place few cancellations in mid-2023 as the economy slowed down. Currently there’s a little appetite for investment as recession fears linger and companies cut CAPEX in 2024.

TW: Are you seeing manufacturers shift their product mixes? Are they moving toward more innovation or are investments more focused on improved efficiency and lowering costs? Engel: Product mixes have shifted from cotton to poly-cotton over the past few years. However, processing types have changed dramatically in the recent past. Ring spinning is becoming less prevalent in the United States (labor intensive) and is moving to areas such as Central America. OE and MVS remain but will not increase in production in the next few years. Most new projects are driven by lowering the cost per pound by reducing labor requirements and improving efficiencies.

TW: Do inflation and higher interest rates create investment headaches? Do you think the United States will avoid a recession? Engel: Elevated inflation and high interest rates have always a dampening effect on investment. The housing market is the biggest loser in such scenarios that weigh on consumer sentiment. As energy/fuel and food prices rise, consumers allocate less disposable income to textiles/apparel and other nondurable goods. With job security still relatively high, consumer confidence is strong. The likelihood of a recession at this point is low, as the overall economy is strong and inflation is trending down. If the FED does not continue to raise interest rates, it would be a sign that we will see some cooling in the next 12 months, but nothing close to a recession.

TW: Are there any roadblocks, such as high energy prices, holding manufacturers back from investing in new equipment and technologies? Engel: The most significant investment roadblocks on a global scale are (1) volatile demand in downstream textile consumption, (2) availability of qualified staff to operate the machines effectively, (3) maintaining cost efficiency and profitability as operating costs (e.g., labor costs) increase. This last factor in particular is proving to be a common barrier for the U.S., as clients continue the trend of investing in Central America to reduce operating labor costs (electricity costs are lower in the U.S. than in Central America), resulting in a shift of production capacity rather than expansion for the American market itself.

TW:What are your thoughts on the impact of artificial intelligence (AI) in textile manufacturing and the technology your company designs/supplies? Engel: In textile manufacturing, AI enables the intelligent analysis of large amounts of data by combining information from different sources to gain new insights. AI can optimize defect detection and product quality, as well as realize predictive maintenance, which will provide our customers with crucial competitive advantages in the future, and significant cost savings per kg produced. In particular, machine learning supports predictive modeling such as quality control, demand forecasting and predictive maintenance.

TW: Can you comment on the quantity and quality of visitors at your booth during the show, and the countries and regions where the visitors came from? Meyer: There was an unexpectedly high number of visitors from all over the world at this year’s ITMA, and especially more customers from Latin America than expected. Generally, all textile manufacturing regions were well represented.

TW: Of the machines/technology your company had on display, what drew the most attention? Meyer: There was a lot of interest in the Montex®Coat, the latest addition to our range of technologies which we displayed in Milan.

The Montex®Coat can serve a very diverse number of markets and enables full PVC coatings, pigment dyeing or minimal application surface and low penetration treatments, as well as solvent coatings. Knife coating, roller coating or screen printing can also all be accommodated with this system.

As such, it provides the ultimate in flexibility and the ability to switch quickly from one fabric run to the next, without compromising on the economical use of energy or raw materials.

Many refinements have been made to the Montex®Coat in the past few years, resulting in higher coating accuracy and the resulting quality of the treated fabrics. A number of advanced new improvements were introduced in Milan, including automatic edge limiters for immediately adapting to new coating widths and a new and simplified hand-held control device. These save considerable time in setting up the machine and ensuring consistent production.

TW: Based on customers’ interests and questions during the show, do you see any overarching trends? In your sector, what impact does sustainability have? Meyer: Monforts Montex stenters for processes such as drying, stretching, heat-setting and coating are already the industry standard for the fabric finishing industry, providing a number of advantages in terms of production throughput and especially in energy efficiency and resource savings.

As finishing is a particularly energy-intensive part of the textile production chain, it is exactly where palpable results can be achieved and we have developed a wide range of energy-saving measures.

This not only includes state-of-the-art machine chamber insulation, but also heat recovery systems. The Monforts Universal Energy Tower, for example, is a free-standing air/air heat exchanger that achieves energy savings of up to 25 percent.

The ECO Booster heat recovery system with integrated automatic cleaning is meanwhile directly integrated into the chamber design of the Montex stenter and enables energy savings of up to 35% depending on the application. One ECO Booster module is sufficient for stenter ranges with up to eight chambers.

Both the ECO Booster and the Energy Tower can be retrofitted to existing ranges, in order to make production more resource-efficient and economical, yet without having to invest in a new machine.

TW: What is the appetite for investing? Is U.S. interest apparent? Meyer: Prior to ITMA 2023, we were expecting this year to be challenging, given the generally gloomy analyst forecasts for the immediate future of the textile industry, so the number of new sales being announced at ITMA 2023 and the upbeat atmosphere took us by surprise.

We have sold a number of machines to companies in Mexico and other Latin American countries who are primarily manufacturing for the U.S. brands. Established manufacturers in the USA are meanwhile looking to replace older installations in order to benefit from all of the latest developments and increased productivity in high-level finishing.

TW: Do recent orders point to any evidence of nearshoring and reshoring in the Western Hemisphere? Meyer: We have certainly seen more investments within Europe during the past two-to-three years, in France, Germany, Spain, Italy and the UK. Where nearshoring and reshoring are happening, it is generally in the upstream fields of digital decoration, printing and garment making-up — the final stages of the supply chain.

TW: Are there any roadblocks, such as high energy prices, holding manufacturers back from investing in new equipment and technologies? Meyer: If anything, high energy prices are having the opposite effect and encouraging investment. For our customers, energy costs can account for up to 70% of production costs, so there is great demand for ways of saving money. This also helps in terms of global warming and reducing carbon footprint, of course.

We see the energy crisis of the past two years as an opportunity because it is leading to an energy consumption rethink in the textile industry.

At ITMA 2023, for example, the two seminars we organized on green hydrogen as a new energy source for textile finishing were very well-attended.

Monforts is currently leading a consortium of industrial partners and universities in the three-year WasserSTOFF project, launched in November 2022, to explore all aspects of this fast-rising new industrial energy option.

The target of the government-funded project is to establish to what extent hydrogen can be used in the future as an alternative heating source for textile finishing processes. This will first involve tests on laboratory equipment together with associated partners and the results will then be transferred to a stenter frame at the Monforts Advanced Technology Center (ATC) in Germany.

Green hydrogen’s potential as a clean fuel source is tremendous, but there is much we need to explore when considering its use in the textile finishing processes carried out globally on our stenter dryers and other machines.

TW: Do you have any forward-looking thoughts as you digest ITMA 2023 and look ahead to Hanover in 2027? Meyer: The textile industry is preparing for the future and wants to contribute to a general reduction in CO2 emissions.

At ITMA 2027 in Hannover we will see what further responses to this major challenge have been realised. In Milan this year it was just good to be back at a physical show and meet many colleagues and customers from around the world. This is something everybody has missed during the past few years.

Thomas Oetterli

Respondent: Thomas Oetterli, CEO Rieter Group, Switzerland

TW: Can you comment on the quantity and quality of visitors at your booth during the show, and the countries and regions where the visitors came from? Oetterli: We were blown away by both the quality and quantity of visitors to our booth. We welcomed many current and prospective customers from around the world, engaging in insightful and in-depth conversations around a shared passion: Rieter technology. In addition, our virtual booth enabled us to share the greatest moments with customers from around the world in real-time, from the unveiling event through to daily product launches.

TW: Of the machines/technology your company had on display, what drew the most attention? Oetterli: Our innovations were well received. Our revolutionary double-sided air-jet spinning machine J 70 drew huge crowds. The machine boasts up to 200 autonomous spinning units and four robots, allowing production speeds of an unmatched 600 m/min.

Interest in our recycling offering is skyrocketing: Com4recycling is the Rieter system that enables customers to produce fine, high-quality ring and compact yarns from challenging raw material. This holds true even with a relatively high proportion of mechanically recycled cotton fibers.

TW: Based on customers’ interests and questions during the show, do you see any overarching trends? Oetterli: All things automation and digitization sparked interest. ROBOspin, the industry’s first fully automated piecing robot, is highly coveted in times of tight labor markets. We are also seeing a growing appetite for digitization services like ESSENTIAL – Rieter Digital Spinning Suite. This indicates that there’s a generational shift underway to younger mill owners for whom digitization is a must-have. This aligns seamlessly with our vision to fully digitize spinning mills.

TW: What role does sustainability play? Oetterli: For a long time, yarns were perceived as a commodity in the textile value chain. But recycling is changing all this, putting yarns at the forefront of the industry’s efforts to become more circular and fight climate change and biodiversity loss. When yarns made from recycled fibers reach acceptable quality levels, this also has positive impacts on downstream processes. Global brands are now turning their focus on spinning to understand the limitations and opportunities in processing recycled fibers. Our in-depth textile expertise is helping customers tap into a unique market opportunity.

TW: What is the appetite for investing? Is U.S. interest apparent? Oetterli: The textile industry is highly cyclical. Markets across the globe have recorded a slowdown since the middle of last year and now a certain restlessness is palpable. Projects are being planned and everyone is waiting for the recovery, but it is hard to pinpoint when it will set in.

TW: Are you seeing manufacturers shift their product mixes? Are they moving toward more innovation or are investments more focused on improved efficiency and lowering costs? Oetterli: In the spinning industry, competitiveness is the name of the game. This is why we design every new machine generation to improve efficiency in terms of energy and raw material consumption. Our latest machine generations are unbeatable in this respect. Highlights include the J 70, our sewing thread finish winder, Thread King, and our new card C 81, to name just a few.

TW: What are your thoughts on the impact of artificial intelligence (AI) in textile manufacturing and the technology your company designs/supplies? Oetterli: We are incorporating artificial intelligence into existing machinery, a case in point is our card C 81, where we have added intelligent sensors which set the carding gap to the ideal size and monitor contaminant content in real-time.

The use of artificial intelligence will make a significant contribution to automation and process optimization and thus to improving sustainability in the textile industry. To expand our leadership in the field of industrial artificial intelligence, Rieter and the Johann Jacob Rieter Foundation are funding a professorship at ZHAW School of Engineering in Winterthur, Switzerland.

TW: Would you say ITMA 2023 was an overall success for your company? Oetterli: It was a resounding success! ITMA 2023 confirms our strategy of advancing our systems approach by incorporating intelligence and engineering performance. Our technology helps customers to capitalize on more market opportunities and produce more economically.

NIRI’s latest white paper explores the challenges and opportunities for sustainable nonwoven product development

TW Special Report

The nonwovens sector embraces innovation and environmental and social responsibility perhaps more than any other industry. As the EU and the U.S. Environmental Protection Agency (EPA) bring in further regulations to restrict the use of per- and polyfluoroalkyl substances (PFAS), we face significant challenges — and the ubiquity of PFAS means these changes will affect industries across the board, from construction to filtration, from medical to food and beverage.

The England-based Nonwovens Innovation & Research Institute Ltd. (NIRI), a nonwoven and textile product development and R&D group, has produced a new white paper outlining the issues, and exploring potential solutions to help customers maintain a competitive edge while addressing the business-critical aspects of sustainability and social responsibility. The white paper offers insights into how new material science and fiber innovation, coupled with pragmatic product design decisions, can reduce dependency on PFAS or eliminate it altogether, without compromising performance requirements.

“Forever chemicals” have been found to pose significant risks. Unintended leakage has led to long-term environmental accumulation, contaminating soil, ground, and surface water, disrupting ecosystems, and impacting the food chain. The propensity of PFAS to bioaccumulate in the body has been linked to chronic diseases and reduced fertility, with exposure linked to kidney, liver, bowel and thyroid diseases and cancers, as well as acute health conditions such as high cholesterol, increasing the risk of stroke or heart attack. As the unconstrained use of PFAS is neither sustainable nor societally acceptable, access to PFAS is becoming increasingly restricted — posing significant and imminent challenges for industrial usage. In 2025, the European Chemical Agency (ECHA)’s recommendation on the restriction of PFAS will pass into law and become part of REACH regulations. This will mean a total ban on the use of many PFAS above a threshold quantity following an 18-month transition period. In parallel, the EPA has introduced strategies and programs to limit human and environmental exposure to PFAS.

The transition away from PFAS is already impacting manufacturers and convertors in the nonwovens sector, as some companies restrict the use of existing stocks to focus on a smaller number of products, leaving some products out of specification and underperforming. In this context, there is an increasingly urgent need to explore options to reduce or eliminate dependency on PFAS and, given the ubiquitous nature of PFAS across a whole host of sectors, the commercial and regulatory demand to find PFAS-free approaches cannot be ignored.

NIRI’s latest white paper outlines their approach to re-evaluating the design and formulation of products to help companies reduce or eliminate PFAS from their products and processes — an approach that has already been harnessed by NIRI and their customers to evaluate how to effectively navigate the transition from PFAS while still achieving required product performance. NIRI’s approach asks one significant question: how can we influence the bulk performance of the product through intelligent design, rather than relying entirely on surface coatings?

The white paper posits the transition away from PFAS as an opportunity — both to ensure new developments are compatible with circular economy approaches, and as a route to re-evaluating and upgrading designs for futureproof products and greater sustainability. With growing customer awareness of social responsibility, companies who respond to the PFAS-free challenge ahead of regulatory deadlines can be ideally positioned to increase market share through premium brand positioning.

Tackling the PFAS issue is just one example of the many sustainability challenges NIRI is helping to address, as a world-class innovation and product development supplier of sustainable materials, fibers, nonwovens, and their associated products. With industry-leading expertise and full prototyping and analytical capability, NIRI accelerate innovation, develop commercially viable products, identify new market opportunities, and provide world-class scientific advisory services for customers from start-ups to multinationals.

NIRI is trusted by global leading innovators to guide and support them with their most critical and game-changing aspirations — from ideating concepts to assisting the transition to upscaled manufacturing. With over 900 projects completed for more than 450 customers across the full spectrum of the nonwoven supply chain, NIRI’s rapid corporate expansion reflects the value and growth provided to customers, worldwide.

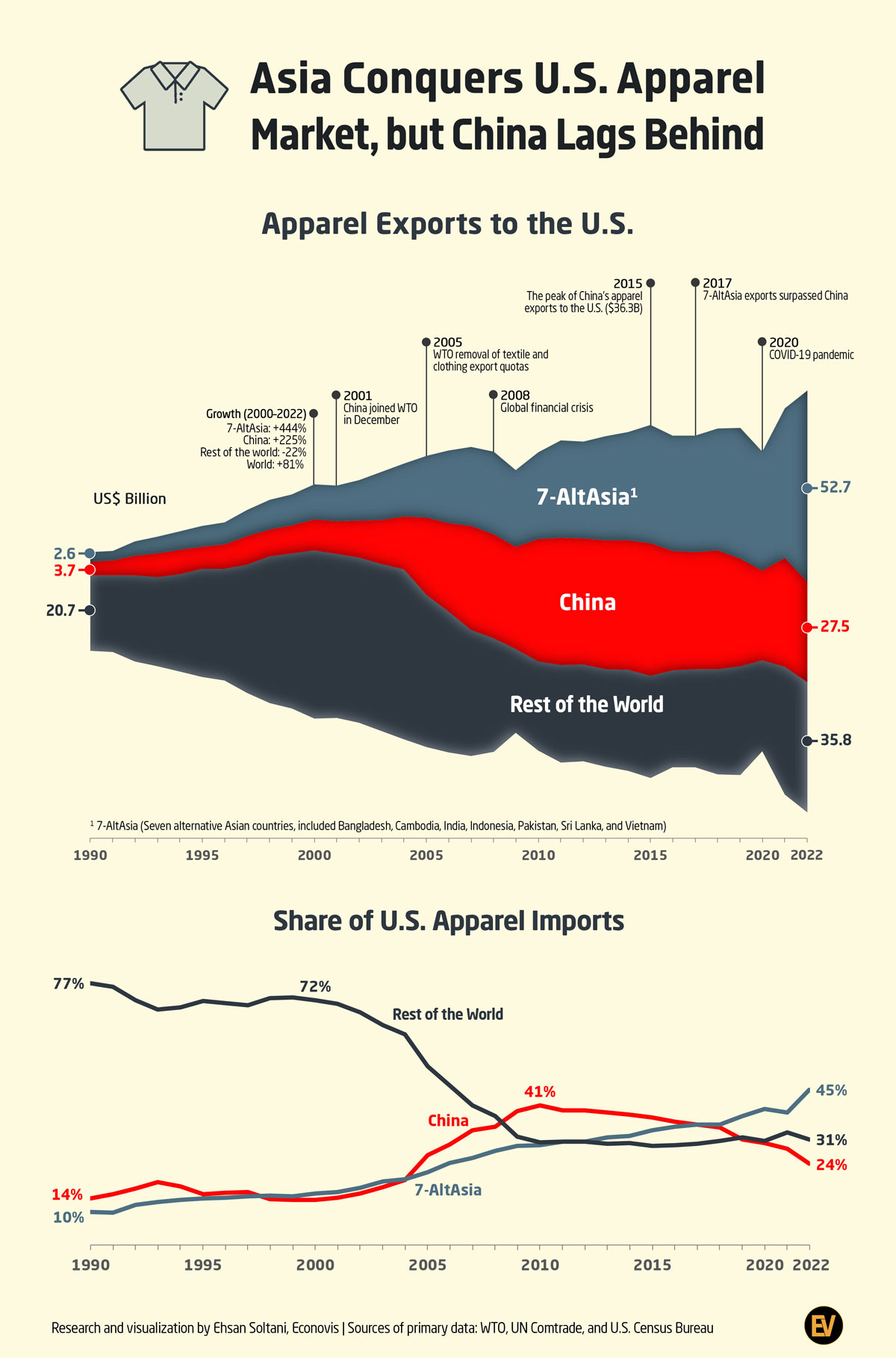

United States apparel imports surged by 81 percent, increasing from $64 billion in 2000 to $116 billion in 2022, while total goods imports grew by 168 percent. The share of apparel from total imports declined from 5.1 to 3.4 percent during this period. Notably, the share of knitted apparel from total woven and knitted apparels rose from 45 percent in 2000 to 58 percent in 2022, indicating an increased preference for more casual apparel imports with lower prices.

From 1995 to 2000, the share of the world, excluding China and seven Altasia countries — Bangladesh, Cambodia, India, Indonesia, Pakistan, Sri Lanka, and Vietnam — in total U.S. apparel imports was around 72 percent. This dominance was attributed to import quotas that protected the U.S. market from cheap Asian exporters.

Two significant turning points unfolded in the 2000s. China joined the World Trade Organization (WTO) in December 2001, and more importantly, from January 2005, quotas on textile and apparel exports were eliminated, marking the removal of all quantitative restrictions on imports from WTO members under the Multi-Fiber Arrangement (MFA), which had been in place for more than four decades.

Apparel exports from the world — excluding China and the seven Altasia countries, which amounted to approximately $46 billion from 2000 to 2004 — experienced a notable decline, falling to $24.6 billion in 2010. In contrast, China’s exports surged by 133 percent, while the seven Altasia countries witnessed a 64-percent increase from 2004 to 2010. As a result, the share of the world, excluding China and the seven Altasia countries, in total United States apparel imports was halved, remaining at around 30 percent throughout the 2010s.

China’s apparel exports to the United States peaked at $36.3 billion in 2015. From 2015 to 2022, China’s apparel exports to the United States decreased by 24 percent, and the seven Altasia countries increased by 62 percent. As a result, China’s share of total U.S. apparel imports dropped from 37.4 percent to 23.7 percent.

In 2022, the seven Altasia countries, with a total export value of $52.7 billion, constituted 45 percent of United States apparel imports. Notably, Vietnam and Bangladesh, with apparel exports amounting to $19.5 billion and $10.3 billion, respectively, surpassed China, whose exports stood at $27.5 billion. Furthermore, India, Indonesia, and Cambodia recorded apparel exports of $6.3 billion, $6.2 billion, and $4.8 billion in 2022, respectively.

The production and export of textiles and clothing played a central role in generating export revenue and fostering economic development in China. Until the mid-2010s, textiles and clothing constituted the primary source of export revenue for China. Notably, textiles and clothing still hold significance for the Chinese economy, with a trade surplus share of 16 percent and 35 percent of total manufacturing and goods exports, respectively, in 2022. However, the apparel share from China’s total goods exports gradually decreased from 20.1 percent in 1993 to 5.1 percent in 2022. Due to industrial and economic development, demographic changes, and a more than threefold increase in labor costs compared to the seven Altasia countries, these nations are poised to gain a larger share in the United States market, while China’s share is expected to continue declining in the future.

Editor’s Note: Ehsan Soltani is with West Lebanon, N.H.-based Econovis LLC

A stable, reactive, and cost-effective ruthenium catalyst for sustainable hydrogen production through proton exchange membrane water electrolysis has been developed by researchers

TW Special Report

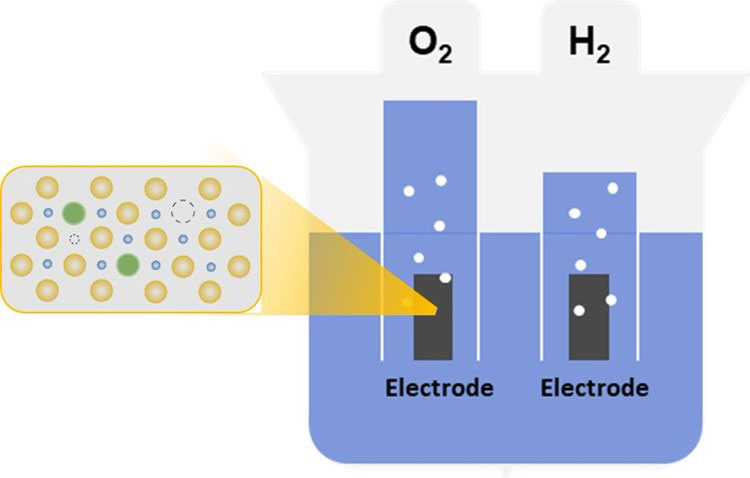

Sustainable electrolysis for green hydrogen production is challenging, primarily due to the absence of efficient, low-cost, and stable catalysts for the oxygen evolution reaction in acidic solutions. A team of researchers has now developed a ruthenium catalyst by doping it with zinc, resulting in enhanced stability and reactivity compared to its commercial version. The proposed strategy can revolutionize hydrogen production by paving the way for next generation electrocatalysts that contribute to clean energy technologies.

Electrolysis is a process that uses electricity to create hydrogen and oxygen molecules from water. The use of proton exchange membrane (PEM) and renewable energy for water electrolysis is widely regarded as a sustainable method for hydrogen production. However, a challenge in advancing PEM water electrolysis technology is the lack of efficient, low-cost, and stable catalysts for oxygen evolution reaction (OER) in acidic solutions during PEM water electrolysis. While iridium-based catalysts are a potential solution, metallic iridium is rare and expensive in nature. Alternately, oxides of ruthenium (RuO2) offer a more affordable and reactive option, but they also suffer from stability issues. Therefore, researchers are exploring ways to improve the stability of the RuO2 structure to develop promising OER catalysts for the successful implementation of the hydrogen production technology.

Now, at study to be published in Volume 88 of the Journal of Energy Chemistry in January 2024, a group of researchers, led by Professor Haeseong Jang from the Department of Advanced Materials Engineering at Chung-Ang University, has developed a promising OER catalyst. Denoted as SA Zn-RuO2, the catalyst comprises of RuO2 stabilized by single atoms of zinc. Elaborating about their study, Professor Jang said: “We were motivated by the need to find efficient and cost-effective alternative electrocatalysts for OER in PEM water electrolysis. Based on our study, we propose a dual-engineering strategy, involving single atom Zn doping and the introduction of oxygen vacancies, to balance high catalytic activity with stability during acidic OER.”

The researchers synthesized SA Zn-RuO2 by heating an organic framework with ruthenium (Ru) and zinc atoms, forming a structure with oxygen vacancies (missing oxygen atoms that positively alter the properties) and Zn-O-Ru linkages. These linkages stabilize the catalyst in two ways — one, by strengthening the Ru-O bonds, and second, by providing electrons from zinc atoms to protect ruthenium from overoxidation during the OER process. Furthermore, the improved electronic environment around the ruthenium atoms lowers the energies needed for molecules to stick to the surface, thus lowering the energy barrier for the reaction.

The resulting catalyst was more stable, with no apparent fall in reactivity, and significantly outperformed commercial RuO2. Moreover, it required less extra energy (low overpotential of 213 mV compared to 270 mV for commercial RuO2) and remained functional for a longer period (43 hours compared to 7.4 hours for commercial RuO2).

Due to its improved stability and features, the newly proposed SA Zn-RuO2 catalyst has the potential to influence the development of cost-effective, active, and acid-resistant electrocatalysts for OER. This, in turn, could help in reducing costs and enhancing the production of green hydrogen, aiding in a shift toward cleaner energy sources and advancements in sustainable technologies.

“We believe that this shift can revolutionize industries, transportation, and energy infrastructure, and contribute to the efforts aimed at combating climate change and fostering a more resilient and environmentally conscious future. This is because accessible green hydrogen can have a transformative impact on societies by mitigating environmental impacts, creating jobs, and ensuring energy security through diversified and sustainable energy solutions,” envisions Professor Jang.

In summary, the highly reactive and catalytically stable RuO2 catalyst for the acidic OER has increased durability and favorable characteristics, and holds immense potential for guiding the design of robust and active non-iridium-based OER electrocatalysts for practical applications!

Reference

Title of original paper: Tuning electronic structure of RuO2 by single atom Zn and oxygen vacancies to boost oxygen evolution reaction in acidic medium

GASTONIA, N.C. — January 31, 2024 — Champion Thread Company, a provider of industrial sewing threads, engineered yarns, and other trim & findings, is celebrating its 45 Years of Service to the Textile and Sewn Products Industries.

“For 45 years, we have demonstrated unwavering commitment to excellence and dedication to our customers,” said CTC President Matt Poovey.

Thanks to a loyal and fast-growing customer base, CTC has expanded from its roots as a small thread distributor into a developer, manufacturer, and marketer of a wide range of products and solutions that are sold on four continents.

Some major CTC milestones include:

1979 – Founded by current CEO Bob Poovey

1999 – Moved/expanded corporate office

2007 – Strategic thread manufacturer acquisition

2009 – Started engineered yarn business

2011 – Opened state-of-the-art flexible mfg facility

2014 – Expanded and opened current HQ location

2016 – Matt Poovey promoted to President

2018 – Opened new warehouse/distribution facility

2019 – Celebrated 40 years of industry service

2020 – Jim Lee promoted to Vice President of Sales

2021 – Launched Renu™ line of 100% recycled thread

2023 – Opened new South Carolina dyehouse

2024 – Celebrating 45 years in business

“Since our founding, we have remained family-owned and operated, and take pride in offering the highest quality goods, competitive prices, and unmatched industry expertise,” Poovey said. “Champion Thread’s longevity in the market can be attributed to our ability to adapt and innovate, while always staying true to our core values. Our understanding of the industry has allowed us to consistently deliver superior products that meet the ever-evolving needs of our customers.”

MILAN — January 31, 2024 — Ermenegildo Zegna N.V. (Zegna Group), owner of the ZEGNA and Thom Browne brands and exclusive licensee for the Tom Ford Fashion business, today announced preliminary unaudited revenues of 1.9 billion euros for the full year 2023, up 27.6 percent year-over-year and up 29.7 percent year-over-year on a constant currency basis, with an organic growth rate of 19.3 percent. Revenues for the fourth quarter of 2023 were 570 million euros, up 40.1 percent year-over-year and up 42.9 percent year-over-year on a constant currency basis, with an organic growth rate of 19.6 percent.

Ermenegildo “Gildo” Zegna, Chairman and CEO of the Zegna Group, said: “I am very proud of the Group’s success over the past year, which is demonstrated by our strong and continued revenues growth. The significant increase in our revenues in 2023, and especially from our network of directly operated stores, is a clear indication that demand for our brands remains healthy, and that we are successfully executing our strategy to increase their desirability and solidify their position as leaders in the luxury market. The continuing improvement in the ZEGNA brand productivity, in particular, is a testament to the strength of our execution, supported by our successful merchandising and CRM. Our integrated supply chain benefits all three of our brands and drives ZEGNA’s leadership in Made-to-Measure and product customization. We are focused on further enhancing our Made-to-Measure and personalization offering with the introduction and ongoing rollout of ZEGNA X, which is empowering our style advisors to further serve our customers using the latest technology.”

Ermenegildo Zegna, Chairman and CEO of Ermenegildo Zegna Group , at the Group’s headquarters, in Milan, Italy, Wednesday, July, 12, 2023. – Francesca Volpi for Financial Times

“While we have seen broad-based strength, I am particularly pleased by the continued growth in EMEA and the very positive performance in the US, which was driven by strong double-digit ZEGNA sales via the retail channel. These strengths, coupled with the rebound in the Greater China Region, are testaments to the soundness of our long-term strategy. Our performance across all our key geographies reflects the plans we set out at our second Capital Markets Day at the NYSE in December 2023 and charts a path forward to reach our medium- term goals even in an environment that remains challenging, with the invaluable contributions of our management team and all our employees across the Group and its brands.”

Recent Highlights

ZEGNA Renews Eyewear Partnership with Marcolin — On January 30, 2024, ZEGNA announced the renewal of its licensing agreement with Marcolin to produce of ZEGNA-branded eyewear, which will now continue through the end of 2030. The renewal continues the strong partnership built between the companies since it was launched in 2015.

ZEGNA 2024 Milan Men’s Fashion Week Show — On January 15, 2024, ZEGNA transformed a large industrial space into an “Oasi of Cashmere” for its Fall 2024 Men’s fashion show in Milan. The presentation showcased new designs from artistic director Alessandro Sartori for the brand’s Oasi Cashmere collection, focusing on elements that can be combined in many ways to reflect each customer’s sense of style. The collection was incredibly well received and praised for the way in which it brought high-quality raw materials to life.

ZEGNA Begins Direct Operations of its Business in Korea — Pursuant to the agreement announced on October 24, 2023 between ZEGNA and its South Korean franchise partner, as of January 1, 2024, the Group began directly operating the ZEGNA Business in South Korea. This involved the conversion of the 16 ZEGNA stores in the region to direct-to-consumer points of sale.

ZEGNA Signs New License Agreement for Fragrances and Cosmetics — On November 6, 2023, ZEGNA announced a long-term license agreement with Give Back Beauty for the creation, production, marketing and distribution of fragrances and cosmetics products under the ZEGNA brand worldwide.

Upcoming TOM FORD FASHION and Thom Browne Fashion Shows — Thom Browne’s FW24 Fashion Show in set to take place in New York on February 14, 2024, and the TOM FORD FASHION FW24 Fashion Show will take place in Milan on February 22, 2024.

Review of Preliminary Unaudited Revenues for the Full Year 2023 and the Fourth Quarter of 2023

For the full year 2023, Zegna Group generated revenues of €1,905 million, an increase of 27.6% year-over-year. On a constant currency basis, revenues grew by 29.7% year-over-year, with an organic growth rate of 19.3%. In the fourth quarter of 2023, the Group generated revenues of €570 million, an increase of 40.1% year-over-year. On a constant currency basis, revenues grew by 42.9%, with an organic growth rate of 19.6% for the period. Revenues growth in the fourth quarter of 2023 accelerated from the 20.8% year-over-year growth reported in the third quarter of 2023 (on a constant currency basis, revenues growth was 25.0% in the third quarter, with an organic growth rate of 11.3% for the same period).

Revenues by Segment

Zegna Segment4: For the full year 2023, revenues for the Zegna segment amounted to €1,322 million, up 12.4% year-over-year and 13.8% year-over-year on a constant currency basis, with an organic growth rate of 19.5%. Revenues for the fourth quarter of 2023 were €385 million, up 15.2% year-over-year and up 17.0% on a constant currency basis, with an organic growth rate of 18.2%. The ZEGNA brand’s strong direct-to-consumer (“DTC”) strategy continued to drive revenues for the segment, more than offsetting lower wholesale revenues that resulted from the planned change to a new drop-based merchandising strategy, whereby some Spring/Summer 2024 deliveries were purposely shifted from 4Q 2023 to 1Q 2024.

Thom Browne Segment: For the full year 2023, revenues for the Thom Browne segment amounted to €380 million, up 14.9% year-over- year and up 18.3% year-over-year on a constant currency basis, with an organic growth rate of 17.8% for the year. Revenues for the fourth quarter came in at €99 million, up 30.2% year-over-year and 35.0% on a constant currency basis, with an organic growth rate of 24.6%. The fourth quarter growth reflected the expansion in the brand’s direct-to-consumer channel, as well as strong wholesale deliveries compared to the low base of 4Q 2022, which was due to a different timing of shipments during the course of 2022, when compared to 2023.

Tom Ford Fashion Segment4: Revenues for the Tom Ford Fashion segment since its consolidation on April 29, 2023, came in at €236 million, of which €97 million was recognized in the fourth quarter of the year, reflecting strong performance during the holiday season.

Inter segment eliminations grew from -€15 million in FY 2022 to -€33 million in FY 2023 mainly as a result of the acquisition of TFI since Tom Ford products revenues, previously recorded in Third Party Brands, are recorded as intercompany starting from April 29, 2023.

Revenues by Product Line

Zegna-Branded Products: For the full year 2023, revenues for Zegna-branded products were €1,109 million, up 20.1% year-over-year and up 22.3% on a constant currency basis, with an organic growth rate of 22.3%. Revenues for 4Q 2023 were €326 million, up 18.8% year-over-year and up 20.9% on a constant currency and organic growth basis. In 2023, luxury leisurewear revenues grew at a faster rate than the brand’s average and now constitute approximately 50% of Zegna-branded product revenues. Footwear also outperformed the brand’s average growth rate and now make up 13% of product line revenues, while formalwear and MTM also continued to see dynamic growth. The growth in Zegna-branded products reflects the desirability of the brand and the strong appeal of luxury leisurewear and shoes supports the Group’s strategy to meet changing consumer needs, while maintaining focus on quality.

Thom Browne: For the full year 2023, revenues for the Thom Browne product line were €378 million, up 14.7% year-over-year and up 18.0% on a constant currency basis, with an organic growth rate of 17.5%. Revenues for 4Q 2023 came in at €98 million, up 29.9% year- over-year and up 34.8% on a constant currency basis, with an organic growth rate of 24.3%. The strong growth came on the back of the brand’s DTC expansion strategy, as well as from the focus on womenswear, which continues to grow at a faster pace and reached 30% of the total Thom Browne’s revenues in FY 2023.

Tom Ford Fashion: For the full year 2023, revenues for the Tom Ford Fashion product line, calculated as of its consolidation on April 29, 2023, came in at €236 million. Revenues for 4Q 2023 came in at €97 million.

Textile: For the full year 2023, revenues for the Group’s Textile product line amounted to €151 million, up 10.4% year-over-year and up 9.4% on a constant currency basis, with an organic growth rate of 9.5%. 4Q 2023 revenues were €42 million, up 13.1% year-over-year and up 12.0% on a constant currency basis, with an organic growth rate of 12.1%. The double-digit growth in Textile revenues was supported in particular by Lanificio Zegna.

Third-Party Brands: For the full year 2023, revenues for the Third-Party Brands product line were €25 million, down 74.1% year-over- year and down 74.2% on a constant currency basis, with an organic growth rate of -17.4%. 4Q 2023 revenues came in at €5 million, down 70.6% year-over-year and down 69.9% on a constant currency basis, with an organic growth rate of -33.5%. The revenues of the Third- Party Brands product line was impacted by the end of the distribution licensing agreement for Tom Ford International5.

Revenues by Channel

Direct-to-Consumer (DTC): DTC revenues for the full year 2023 amounted to €1,265 million, up 37.8% year-over-year and up 42.1% on a constant currency basis, with an organic growth rate of 24.5%. DTC revenues made up 66.4% of Group revenues in FY 2023, up from 61.5% in FY 2022. Of that, €945 million came in from Zegna-branded products, up 22.4% year-over-year and up 25.4% on a constant currency basis and organic growth. This reflects strong double-digit growth across all markets thanks to significant productivity gains in all the quarters of the year, and the contribution of 14 net DTC openings to reach a total of 253 DTC monobrand stores as of December 31, 2023. Revenues from Thom Browne DTC amounted to €183 million, up 25.9% year-over-year and up 34.1% on a constant currency basis, with an organic growth rate of 19.7%, reflecting, among other factors, the shift of the South Korean business from wholesale to DTC and an additional six net new openings to reach a total of 86 DTC monobrand stores as of December 31, 2023. Tom Ford Fashion contributed €136 million in DTC revenues since its consolidation on April 29, 2023.

For 4Q 2023, DTC revenues amounted to €400 million, up a significant 46.3% year-over-year and up 50.6% on a constant currency basis, with an organic growth rate of 24.3%. This represented an acceleration from the third quarter organic growth rate of 12.9%, mainly driven by the ZEGNA brand. Zegna-branded products contributed €284 million in DTC revenues in 4Q 2023, up 23.4% year-over-year and up 26.3% on a constant currency and organic growth basis (compared with 14.0% in 3Q 2023), sustained by strong double-digit same store sales growth in most geographies, including a nearly 40% increase in the Greater China Region. DTC revenues for Thom Browne in 4Q 2023 came in at €57 million, up 33.0% year-over-year and up 41.4% on a constant currency basis, with an organic growth rate of 13.3%. For 4Q 2023, Tom Ford Fashion DTC revenues were €58 million.

Wholesale: Wholesale revenues for the full year 2023 amounted to €635 million, up 11.3% year-over-year and up 10.7% on a constant currency basis, with an organic growth rate of 9.6%. Of that, €164 million came in from Zegna-branded products, where wholesale revenues were up 8.4% year-over-year and up 7.0% on a constant currency and organic growth basis. Thom Browne wholesale revenues reflected the conversion of the South Korean points of sales from wholesale to DTC on July 1, 2023, and came in at €195 million for the year, up 5.8% year-over-year and up 6.0% on a constant currency basis, with an organic growth rate of 15.7%. Since its consolidation on April 29, 2023, Tom Ford Fashion wholesale revenues were €99 million. Third-Party Brands and Textile contributed €176 million, down 24.8% year-over-year and down 25.5% on a constant currency basis, with an organic growth rate of 5.8%.

For 4Q 2023, Group wholesale revenues came in at €169 million, up 27.6% year-over-year and up 27.5% on a constant currency basis, with an organic growth rate of 8.9%. Zegna-branded products wholesale revenues for 4Q 2023 amounted to €42 million, down 5.5% year-over- year and down 6.5% on a constant currency and organic growth basis. The drop was mainly attributable to the conversion from wholesale into retail of the Saks Fifth Avenue New York location, and to the planned shift to a drop-based merchandising strategy, whereby a portion of planned Spring/Summer 2024 deliveries were purposely shifted from 4Q 2023 to 1Q 2024. Thom Browne wholesale revenues for 4Q 2023 came in at €41 million, up 25.8% year-over-year and up 26.5% on a constant currency basis, with an organic growth rate of 39.7%. Thom Browne’s wholesale revenues reflected the low base of 4Q 2022, which was due to a different timing of shipments during the course of 2022, when compared to 2023, while being also affected by the South Korean business being moved from wholesale to retail after its internalization. Tom Ford Fashion wholesale revenues for the quarter came in at €38 million. Third-Party Brands and Textile contributed €48 million in 4Q 2023, down 14.2% year-over-year and down 14.3% on a constant currency basis, with an organic growth rate of 4.1%.

Revenues by Geography

Revenues for both the full year and the fourth quarter of 2023 were strong across all key geographies, with double-digit growth across all regions compared to 2022. The most significant growth was reported in North America, which saw revenues grow by 41.6% year-over-year for the full year and 60.1% year-over-year for the fourth quarter, also supported by the consolidation of Tom Ford Fashion.

For the full year 2023, revenues in EMEA amounted to €659 million, up 26.6% year-over-year and up 27.7% on a constant currency basis, with an organic growth rate of 18.8%. 4Q 2023 revenues in EMEA came in at €184 million, up 30.9% year-over-year and up 32.7% on a constant currency basis, with an organic growth rate of 14.2% supported by the strong growth of the Zegna-branded products in the DTC channel slightly offset by more muted wholesale reflecting the already mentioned new merchandising strategy. Activity in Europe remained dynamic throughout the year reflecting strong activity for both domestic and foreign consumers. The UAE continued to outperform the rest of the region, recording revenues for the full year 2023 and 4Q 2023 of €69 million and €24 million, respectively, up 35.0% year-over-year for the full year and 22.4% year-over-year for the quarter. Growth on a constant currency basis was 38.2% and 26.7%, and organic growth was 30.9% and 20.2%, respectively for the full year and the fourth quarter 2023.

For the full year 2023, revenues in North America came in at €417 million, up 41.6% year-over-year and up 40.4% on a constant currency basis, with an organic growth rate of 11.4%. Revenues from the U.S. were €385 million, up 42.3% year-over-year and up 40.9% on a constant currency basis, with an organic growth rate of 10.4%. North America revenues for 4Q 2023 were €132 million, up 60.1% year- over-year and up 60.9% on a constant currency basis, with an organic growth rate of 3.2%. Of that, the U.S. contributed €125 million, up 63.4% year-over-year and up 64.4% on a constant currency basis, with an organic growth rate of 4.4%. The organic growth rate was in the high-teens for Zegna-branded products DTC, partly offset by lower wholesale in 4Q 2023, as a result of the impact of the aforementioned shift in wholesale deliveries, and the conversion from wholesale into retail of the Saks Fifth Avenue store in New York. Despite a volatile consumers backdrop, the significant growth in the U.S. – where spending on ZEGNA is almost double pre-pandemic levels – speaks to the success of the ZEGNA One Brand strategy and execution. It is also due to the resilience of the Group’s ultra-luxury offering and the continuing and growing desirability of our brands.

For the full year 2023, revenues in APAC were €788 million, up 22.2% year-over-year and up 27.3% on a constant currency basis, with an organic growth rate of 23.7%. Of that, €596 million came from the Greater China Region, up 20.5% year-over-year and up 25.7% on a constant currency basis, with an organic growth rate of 24.2%. Japan also showed significant growth, with revenues of €85 million, up 29.9% year-over-year and up 39.8% on a constant currency basis, with an organic growth rate of 28.3%. In the fourth quarter, APAC revenues were €241 million, up 39.0% year-over-year and up 44.3% on a constant currency basis, with an organic growth rate of 32.0%. 4Q 2023 revenues from the Greater China Region amounted to €176 million, up 35.0% year-over-year and up 39.3% on a constant currency basis, with an organic growth rate of 36.1%, thanks to the ZEGNA One Brand strategy execution and also as a result of the adverse impact of Covid-19-related restrictions in 4Q 2022. 4Q 2023 revenues from Japan came in at €26 million, up 27.0% year-over-year and up 39.6% on a constant currency basis, with an organic growth rate of 20.7%.

For the full year 2023, revenues in Latin America were €38 million, up 25.6% year-over-year and up 16.2% on a constant currency and organic growth basis. 4Q 2023 revenues came in at €13 million, up 29.6% year-over-year and up 20.9% on a constant currency and organic growth basis.

Outlook

At its second Capital Markets Day, held on December 5, 2023, in New York City, the Group announced its updated financial goals for the medium term. Within this time frame, the Group is aiming to deliver over 10% compounded annual revenues growth and an Adjusted EBIT CAGR of around 20%, compared to FY 2023. This is expected to generate significant cash surplus even while taking into consideration higher, targeted investments in marketing and capital expenditure to enhance brand desirability and drive growth. The Group’s medium- term targets assume no major future worsening of the global geopolitical, health, macroeconomic and financial markets situation, and no other unforeseen events.

DECATUR, Ala. — January 29, 2024 — Toray Composite Materials America Inc., a manufacturer of advanced composites, celebrates the commissioning of the upgraded carbon fiber production line in its Decatur, Ala., facility. The $15 million upgrade doubles the production capacity of the TORAYCA™ T1100 carbon fiber and adds critical redundancy to support the rising demand for defense applications. Toray’s T1100 carbon fiber is vital to several United States Department of Defense (DoD) weapons systems and the Future Vertical Lift (FVL) program.

Congressman Dale Strong of the Fifth Congressional District of Alabama delivered the event’s opening remarks and highlighted Toray’s contributions to national defense. “I am thrilled to see Toray’s commitment to investments in Decatur and North Alabama. Toray provides high performance carbon fibers which are critical to our defense industrial base and national security. I want to thank them for their investment in Alabama and wish them continued success,” said Congressman Strong.

Major General Tom O’Connor, commanding general of the U.S. Army Aviation and Missile Command, participated as the featured guest in a policy discussion led by former Commander of the Army Material Command, retired General Paul Kern. The discussion focused on the importance of a strong domestic industrial base following the January 11, 2024 release of the Department of Defense’s inaugural National Defense Industrial Strategy (NDIS).

Other esteemed guests included a cross-section of local and federal government, industry, and academia.

Toray has already begun production utilizing this new capability and are in the process of qualifying the new line with a number of customers. “Our team in Decatur worked tirelessly to advance the commissioning of our upgraded carbon fiber production line to support the strong demand from the defense industry. As the DoD prioritizes developing a resilient supply chain as part of the NDIS, Toray’s focus is to ensure that we are doing our part to produce and increase material availability for various defense programs,” said Dennis Frett, President of Toray Composite Materials America.

Toray is the largest carbon fiber and prepreg producer in the United States. The Decatur Plant has operation lines from precursor to carbon fiber and is one of three Toray manufacturing facilities. The company has other locations in Tacoma, Washington, and Spartanburg, South Carolina, producing precursor, carbon fiber, and prepreg. Toray’s comprehensive portfolio of carbon fiber composite materials supports customers in aerospace and defense, industrial, and automotive industries.

SAN FRANCISCO — January 29, 2024 — Levi Strauss & Co. announced that Michelle Gass has assumed the role of president and CEO, as previously disclosed in December. Gass follows Chip Bergh, who served as the company’s president and CEO for the previous 12.5 years. Gass brings extensive retail and omnichannel experience to LS&Co.’s top job and is expected to drive a strategic vision focused on accelerating international growth, positioning the Levi’s® brand as a head-to-toe denim lifestyle apparel business and transitioning LS&Co.’s operating model to a direct-to-consumer (DTC)-first organization.

Today, Gass announced that LS&Co. is expanding its executive leadership team with two immediate appointments, emphasizing the company’s dedication to pivoting fully to a DTC-first, brand-led business model. Levi’s Chief Marketing Officer Kenny Mitchell and newly promoted Chief Merchandising Officer Dawn Vitale will join the executive leadership team, which, under Gass’ leadership, is responsible for setting the company’s overall direction and overseeing all major strategic, financial and operational decisions. In addition, Gass announced the company’s plans to hire a president and chief commercial officer who will join the executive leadership team and be responsible for shaping our global commercial strategy and accelerating growth and profitability for the Levi’s® brand. These changes reflect Gass’ commitment to prioritizing growth and a consumer-centric approach throughout LS&Co.

“I’m thrilled and honored to guide Levi Strauss & Co. into its next era of growth. LS&Co. is a destination for the very best talent because of its history, its products and its values, and this past year I’ve had the unique opportunity to immerse myself in the business and meet so many members of our exceptional teams around the world. I cannot wait to see what we achieve together,” Gass said. “The addition of Kenny Mitchell and Dawn Vitale, as well as our new CEO of Beyond Yoga, Nancy Green, brings decades more of proven retail and consumer obsession to an already strong executive leadership team. I’m confident we have the right executive team and company strategies to accelerate our pivot to become a high-performing, DTC-first company.”

Kenny Mitchell, Levi’s chief marketing officer: Mitchell brings more than 20 years of global brand-building experience to the Levi’s® brand. He joined LS&Co. in 2023 from Snap, parent company of Snapchat, where he served since 2019 as chief marketing officer and led the growth of the platform’s global community, advertising base and developer partners.

Dawn Vitale, chief merchandising officer: Vitale is an accomplished senior merchandising executive with more than 20 years of experience in apparel category development and market expansion across international wholesale and retail channels. Prior to joining LS&Co. in 2018, she served as vice president of Tommy Jeans and head of merchandising for Calvin Klein jeans at PVH Corp., where she helped to introduce the brands to new consumers and build market share.

CARY, NC — February 1, 2024 — INDA, the Association of the Nonwoven Fabrics Industry, announced that exhibit space reservations for IDEA®25 are rapidly approaching 70 percent capacity. INDA encourages all potential exhibitors to make their reservations as soon as possible to ensure they receive the best location for their booth. IDEA is being held April 29-May 1, 2025 at the Miami Beach Convention Center in Miami Beach, Florida.

CARY, NC — February 1, 2024 — INDA, the Association of the Nonwoven Fabrics Industry, announced that exhibit space reservations for IDEA®25 are rapidly approaching 70 percent capacity. INDA encourages all potential exhibitors to make their reservations as soon as possible to ensure they receive the best location for their booth. IDEA is being held April 29-May 1, 2025 at the Miami Beach Convention Center in Miami Beach, Florida. Global suppliers and manufacturers who exhibit at IDEA will connect their technologies and innovations to C-suite leaders, R&D developers, and specifiers. Exhibitors can demonstrate their products to participants from around the world, answer their technical questions, and collaborate on new products.

Global suppliers and manufacturers who exhibit at IDEA will connect their technologies and innovations to C-suite leaders, R&D developers, and specifiers. Exhibitors can demonstrate their products to participants from around the world, answer their technical questions, and collaborate on new products.