ITALIAN RAPIER LOOM TARGETS QUALITY FAbrICSPromatech, the Italian textile machinery group that comprises the Somet and Vamatex weaving machine brands, has launched a new flexible rapier loom. The Somet Alpha will be targeted initially at high-quality fabric producers in Europe and Asia, with its commercial debut in the U.S. scheduled for early next year. The machine is claimed to offer an “incomparable relation between flexibility and speed,” with its development brief having focused on versatility, reliability, ergonomics, the use of advanced technology, and lower running costs.Fuller details of the machine, and an update on the Promatech group recent purchaser of Sulzer Textil — will be published in our next issue.October 2001

Federal Reserve, Consumers Key To Future

Eighth Rate Cut Not Likely To Be Last

Evidence from the latest set of economic reports shows the U.S. economy weakened further in

August, and in the aftermath of the terrorists’ attacks, a recession is likely to be already in

progress. On the bright side, consumers keep spending, and the Federal Reserve stepped in with a

one-half-point cut in short-term interest rates. Further rate reductions are likely to follow to

prevent the economy from going into a deep recession.

The jobless rate increased to 4.9 percent in August from 4.5 percent in July. This climb was

the sharpest monthly increase since early in 1995. Nonfarm payrolls declined by 113,000, despite a

gain of 72,000 jobs in the service sector. Since March, total nonfarm employment is down by 323,000

jobs. With factory output down and a declining business investment, manufacturers slashed 141,000

jobs in August, bringing the total losses from a year ago to more than one million jobs.

Manufacturing employment is at its lowest level since 1964 — a sign that the weakness in U.S.

economic activity has turned into a recession.

The Producer Price Index for finished goods rose 0.4 percent in August, after dropping 0.9

percent in July. The increase was due to a 1.1-percent rebound in energy prices following a 5.8

percent drop in July. Excluding food and energy, the price index slipped 0.1 percent in August,

after rising 0.1 percent in July.

Consumer Energy Prices Continue Decline

Consumer prices edged up 0.1 percent in August, after falling 0.3 percent in August. Energy

prices fell 1.9 percent in August on top of a 5.6 percent drop in July. Core inflation was up 0.2

percent for the second month in a row.

Industrial production dropped by 0.8 percent in August, after edging down 0.1 percent in

July. July’s figures had raised hopes that manufacturing was on the verge of a rebound. The monthly

decline was the 11th in a row, matching the longest stretch of industrial output weakness, which

occurred in 1960. The operating rate of industrial capacity fell to 76.2 percent from 76.9 percent

in July, the lowest level since July 1983.

With consumer confidence down, new housing construction fell 6.9 percent in August to 1.527

million starts.

The U.S. trade deficit of goods and services narrowed in July to $28.83 billion from $29.07

billion

in June. Both exports and imports declined, reflecting economic conditions in the U.S. and

abroad. Exports fell 2.5 percent to $83.73 billion, while imports came down 2.1 percent to $112.56

billion.

Business sales bounced 0.4 percent in July, after falling 1.5 percent in June. Meanwhile,

business inventories eased 0.4 percent. As a result, the July inventory-to-sales ratio edged down

to 1.42 in July from 1.43 the previous month.

Mixed Results Show Textile Output, Utilization Rate Rebound

Producer prices of textiles and apparel were unchanged in August after edging down 0.1 percent

in July. Prices jumped 1.9 percent for greige fabrics and rose 0.2 percent for home furnishings.

However, prices came down 0.4 percent for processed yarns and threads, fell 0.9 percent for

finished fabrics, declined 1.0 percent for synthetic fibers and dropped 1.3 percent for carpets.

Results for textiles and apparel were mixed. The industry’s payrolls declined 0.2 percent in

August, after falling 1.1 percent in July. The volatile jobless rate for textile mill workers came

down to 8.3 percent from a high of 9.1 percent in July.

Textile output increased 0.8 percent in August, after falling 2.4 percent in July. Output was

13.8 percent below the year ago level. The utilization rate for textiles moved up to 71.6 percent

of capacity from 70.8 percent in July.

Shipments by textile producers declined 0.8 percent in July after rising 1.7 percent in June.

Inventories were pared down by 1.3 percent. As a result, the inventory-to-sales ratio edged down to

1.66 from 1.67.

U.S. retail sales rose 0.3 percent in August, paced by sales gains of 1.2 percent at gasoline

stations, 0.9 percent at building materials and supplies stores and 0.6 percent at department

stores. Sales eased 0.2 percent for motor vehicles and parts and edged down 0.1 percent at

furniture and home furnishings stores. At apparel and accessory stores, sales declined 0.8 percent

in August after rising 1.0 percent in July.

October 2001

Lantech Designs Automated Turntable Wrapping System

Lantech, Louisville, Ky., has designed the Q-1000 Automated Turntable Wrapping System with added

protection for operators.The system features an in-feed and exit conveyor separated by a turntable

that rotates while stretch film is attached to the load. Film loading of the roll carriage is from

the side, providing unobstructed access and ergonomically sound operation.The roll carriage is

safety-guarded to prevent hand injuries. Transition photocells are mounted on either side of the

turntable for easy access. If a photocell beam is broken during wrapping, the machine will shut

down immediately.The E-Z Thread® roll carriage provides loading with no threading required. All

controls are adjustable from the color-coded control panel without the use of a plug-in external

computer.

October 2001

Steel Heddle Files Chapter 11 Sells Textile Business

Steel Heddle Files Chapter 11,Sells Textile BusinessSteel Heddle Group Inc. and its U.S. subsidiaries, including its primary operating entity, Steel Heddle Manufacturing Co. Group Inc., Greenville, S.C., has voluntarily filed a reorganization case under Chapter 11 of the U.S. Bankruptcy Code in the Delaware Bankruptcy Court. The petition was filed, in part, to consummate the sale of the textile business, which includes the textile loom accessories manufacturing and design operations.Steel Heddle is also completing negotiations for a Debtor-in-Possession (DIP) financing facility.Robert W. Dillon, president and CEO, said that with the DIP financing in place, Steel Heddle should be able to consummate its going-concern sales; meet its going-forward obligations to employees, customer and vendors; and ensure a smooth transition of its operations to the purchasers.October 2001

TYAA Photo Flash Report

Outgoing President Charlie King (left), Unifi Inc., receives a recognition plaque for his

2000-2001 term from TYAA past president John Amirtharaj, Universal Fiber Systems LLC.

Charlie King (left), congratulates the new 2001-2002 TYAA President, Robert Howell, general

manager, Dillon Yarn Corp.

TYAA members stayed busy and exchanged thoughts during the breaks in the conference

room. held its summer conference July 26-28 in Myrtle Beach, S.C. The general

theme of this year’s meeting was Strategy Beyond Survival. As the title suggests, the

entire U.S. textile industry is presently going through some very trying times, and several

papers covered this topic.Kay Norwood, senior vice president and textile analyst for Wachovia

Securities, explained there is not much hope that the domestic textile industry will return

to the level that was experienced just a few years ago. Norwood pointed out that the

strong dollar value in comparison to other world currencies encourages imports even

more and makes it difficult to export on a competitive price/performance level.Trade

quotas presently in place with Asian countries will be eliminated in 2005, including quotas

for China upon its entry into the World Trade Organization (WTO). Norwood advised that fiber,

yarn and fabric manufacturers must interact through strong partnerships, find niche

markets and manage their inventories efficiently.Alasdair Carmichael, associate

consultant, PCI Group FibresandRaw Materials, Spartanburg, S.C., pointed out that not

everything happening in the U.S. textile industry is negative. Aside from unfortunate plant

closings and layoffs, he presented many positive elements.Deliveries of texturing spindles to the

United States ranked second-highest in the world in 2000. U.S. exports of textured polyester exceed

imports.Several overseas investments have been made in the U.S. textile manufacturing

industry.Domestic investments continue to be made in the industry.Carmichael explained that factors

such as the value of the U.S. dollar, U.S. consumer demand and fashion, as well

as raw-material costs influence the import situation quite significantly. The biggest

concern is that China has been gearing up with capacity increases and continues to

install modern production equipment. Carmichael foresees another significant boost of apparel

exports by China in 2005 due to its entry into the WTO.

Kay Norwood, senior vice president,Wachovia Securities, talked about thepresent and upcoming

challengesthat are facing the U.S. textile industry.

Alasdair Carmichael, associate consultant,PCI FibresandRaw Materials, talked about

thepositive aspects of the U.S. textile industry.

October 2001

Newly Private Springs Coteminas Form Alliance

Newly Private Springs,Coteminas Form AllianceSprings Industries Inc., Fort Mill, S.C., has entered into a long-term, strategic alliance with Brazil-based Coteminas for bed and bath products.Coteminas will support Springs sales and marketing of home furnishings products in North America with its manufacturing resources.Crandall C. Bowles, Springs chairman and CEO, commented on the alliance: Supplementing Springs manufacturing capabilities with Coteminas world-class textile facilities will allow us to offer a broader array of products on a competitive basis. Springs relationships in the marketplace, well-known brands and distribution capabilities will ensure that our alliance with Coteminas provides more opportunities for all of our customers.In other news, Springs announced the completion of its going-private proposal. As a result of a recapitalization merger between the Close family and an affiliate of Heartland Industrial Partners LP, each outstanding share of Springs common stock held by public shareholders has been converted into the right to receive $46.00 in cash.October 2001

ASTM To Develop Standards For Protective Garments

The American Society for Testing and Materials (ASTM) Committee F23 on Protective Clothing, West

Conshohocken, Pa., is developing new standards to evaluate the effects of protective garments on

humans in hot environments. An ASTM Human Factors Subcommittee will focus on factors associated

with protective clothing worn to prevent heat stress in hot, warm or humid conditions.The

subcommittee has established bench-scale and manikin-based test methods and practices to evaluate

the insulative effects of protective clothing material and garments. It now seeks new members or

input as it develops a methodology related to heat-stress incidence.The subcommittee proposes two

standards: (1) a Standard Guide for Conducting Evaluations of the Heat Stress Effects for

Protective Clothing; and (2) a Standard Practice for Evaluating the Effectiveness of Personal Body

Cooling Garments (or Devices).Those interested in participating should contact Elizabeth A.

McCullough, professor, Institute for Environmental Research, Kansas State University, Manhattan,

Kan.; (785) 532-2284; e-mail: lizm@ksu.edu.

October 2001

Add Value Or Else

Add Value Or Else

A Caribbean Basin Initiative strategy for U.S. mills Despite all the high hopes and

hoopla surrounding the passage last year of the Caribbean Basin trade legislation, the results,

thus far, have been disappointing for most U.S. mills producing apparel fabrics or yarns. There is

little doubt that imports of apparel products from the region will grow over the next few years.

The real question is whether the Caribbean Basin Initiative (CBI) region can compete in the long

term with other apparel-producing regions especially after the quotas are removed on apparel

imports from other countries in 2005.For producers of apparel fabrics and yarns, this situation is

particularly critical. Like it or not, U.S. apparel production will continue to decline, and

imports of finished garments will continue to increase. Even the most competitive U.S. producer of

apparel fabrics or yarns will find it hard, if not impossible, to prosper without a competitive

downstream customer.The other cold reality is that retailers and wholesalers of apparel products

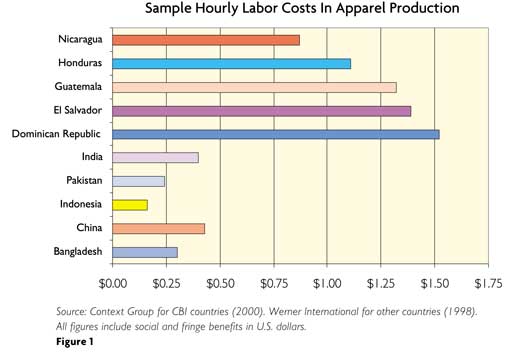

will always be forced to chase the cheap needle. And even though labor costs today are considerably

lower in the CBI region than in the United States they are still considerably higher than in other

less-developed countries in Southeast Asia, the Indian Subcontinent and Africa.

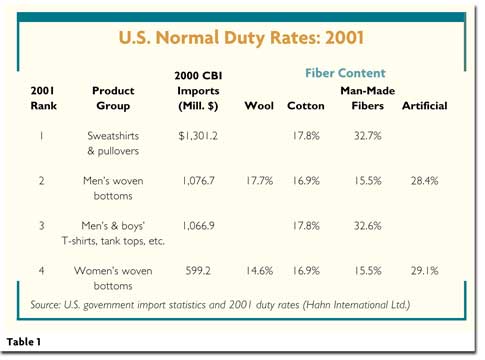

Elimination Of Quotas Will Reduce CBI AdvantageBy far, the biggest and most important

advantage for the CBI region is in the zero-duty rate on qualifying garments, i.e. those made from

U.S. fabrics and yarns. Currently, that advantage is significant in many key product

classifications when compared to the duty rates on imports from Asia and other regions.Figure 1

shows the top imports from the CBI region in 2000 and the duty rates that would apply to the same

garments imported from China, India or most other countries.Unfortunately for the CBI region (and

Mexico), the elimination of import quotas (not duties) on other countries in 2005 will cut deeply

into that competitive advantage.For most imports still covered by U.S. quota restrictions and that

includes most apparel products there is frequently a cost associated with acquiring the export visa

in the supplier country. The quota cost if there is one is usually reflected in the f.o.b. cost of

the garment from the foreign manufacturer. The cost of quota can vary significantly from country to

country, depending on U.S. market demand for the product, the capabilities of manufacturers in a

particular country, and the quantity of quota available in that country for that quota year. Quota

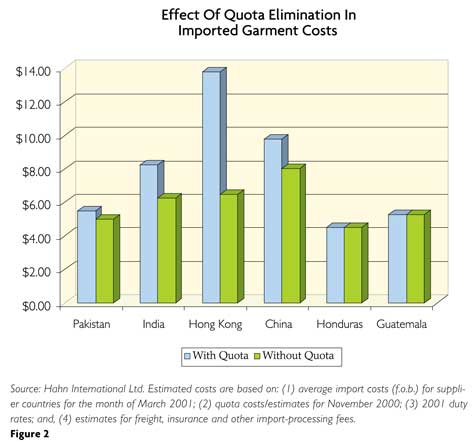

costs also rise and fall during the quota year.In some countries such as Hong Kong and China the

quota charge can be significant.Figure 2 illustrates the before and after impact of the elimination

of import quotas on one important product classification mens cotton polo shirts.Its clear from

this example that factories producing polo-style shirts in the CBI region could easily find

themselves after 2005 at a competitive disadvantage with producers in lower-cost countries such as

Pakistan and for moderate- to better-quality polo shirts from countries such as Hong Kong, China

and India. The same, of course, applies to other products as well.

CBI Region Lacks Packaging Infrastructure Or FacilitatorsAnother challenge facing the CBI

region is the growing demand for full-package garment production from U.S. wholesalers and

retailers. Unfortunately, few independent garment factories in the region have the capability to

offer full-package services due to financing limitations, lack of knowledge about U.S. fabric and

trim sources, inadequate pattern-making or fabric-cutting capabilities, and other critical elements

of full-package production. Likewise, few independent factories in the region can offer the type of

product development support or quick turnarounds on samples or pricing as can their Asian

competitors.While there are some U.S. companies such as Perry Ellis International, VF Corp.,

Kellwood, Tropical Sportswear and others that can effectively facilitate or manage full-package

production in the region, theres room for more. Although the Asians are well-represented with

factories in the region, most of the fabric and trim purchasing and other coordination/facilitation

is done through their Asian offices which puts U.S. mills at a disadvantage.The situation begs for

more facilitators or aggregators to step in and fill this role. The recent formation of the

Amerisource Group is a step in the right direction. Hopefully, for U.S. mills, others will

follow.

Long-Term Strategy: Add ValueFor the short term, U.S. producers of apparel fabrics and yarns

have little choice but to focus on those product groups in which North American producers are

currently the most competitive bottom-weight cotton fabrics and basic cotton knits for T-shirts,

sweatshirts and underwear. However, for the longer term, U.S. mills are going to need a different

approach in order to prosper.1.Focus on higher-value fabrics.With CBI labor costs already high in

relation to other lower-cost countries such as Pakistan, India and Bangladesh, its critically

important for the long term to reduce the labor-cost component in garments produced in the region

without lowering the value of the product. The best way to do that is to increase the value of the

fabric in the garment.Finding ways to increase the use of better-quality wool and synthetic fabrics

in mens and womens dress slacks would be one example of a strategy that could work for the

region.2.Forge alliances with best-of-class knitters and finishers.The lack of knitting capacity in

the CBI region is proving to be a real obstacle for U.S. yarn spinners. Yarn spinners should be

forging alliances with top-quality U.S. knitters to do full-package production of better-quality

knit garments in the CBI region, or else looking for an Asian partner that is willing to build a

knitting plant in the region. Likewise, U.S. greige weavers need to partner with best-of-class U.S.

finishers to produce better-quality bottom-weight or shirting fabrics.3.Upgrade the capabilities of

CBI factories.Using the best fabrics alone will not be enough if the CBI region cannot meet the

quality standards or price points of U.S. retailers and wholesalers. Just looking at the list of

top imports from the region, one sees the current focus on basic, relatively low-labor-content

products like T-shirts, jeans and underwear. Unless factories can upgrade their sewing skills and

productivity over time, they will be displaced by new low-cost suppliers in other regions.U.S.

mills need to be identifying and partnering with factories in the region that have the will and the

resources to upgrade their capabilities. In many cases, these will be Asian-owned plants with

headquarters in Asia. Calling on those factory owners should be a top priority. Making the economic

case for the use of U.S. fabrics in CBI production will also be required.4.Find the

aggregators.Likewise, U.S. mills need to be forging alliances with U.S. and Asian aggregators doing

production in the CBI region. These companies can bring the essential sourcing network, logistical

and financing capabilities, product development support, and most importantly the customers to the

table.5. Develop product sourcing infrastructure and outsourcing capability.Last but not least,

U.S. yarn spinners, knitters and weavers should not put all of their eggs in the CBI basket. While

the CBI region and Mexico can provide economical alternatives to U.S. apparel production, the

strict rules of origin requiring the use of U.S. fabrics and yarns can be both a blessing and a

curse. In order to reduce costs, move up the value chain and meet the future needs of U.S.

retailers and wholesalers, U.S. mills are, in some cases, going to have to supplement their use of

local yarns and fabrics with imported products.Using imported yarns, however, does not necessarily

rule out the possibility of lower-cost apparel production in North America. Under NAFTA rules, sewn

product assembled in Mexico can still qualify for full NAFTA benefits zero duties and no quotas as

long as the fabric is formed and cut in the U.S. This rule creates opportunities to use imported

yarns to upgrade a knit or woven fabric and still meet the pricing requirements of a U.S.

wholesaler or retailer.

Editors Note: Jim Langlois is executive director of Hahn International Ltd., Stamford, Conn, a

company that helps its industry clients develop and execute strategies to stimulate growth and

profitability in the North American market.Hahns team of senior professionals and strategic

alliances with other industry specialists bring strategic planning, market research methodologies

and access to top executives throughout the fiber, textile, apparel and retail supply chains. The

company has extensive hands-on experience in production, marketing, importing and exporting of

textile-related products. For more information visitwww.hahninternational.com.

October 2001

KoSa Introduces New Yarn Products

Charlotte, N.C.-based KoSa has added three new polyester yarns to its product line.Imbue has

antimicrobial properties furnished by an imbedded silver ceramic additive that provides lifetime

resistance to the development of bacterial and fungal growth. Imbue is targeted for use in

performance and fashion apparel, as well as in home furnishings, medical, hospitality and

industrial applications.Stretch-aire®, a single, atmospherically dyeable yarn, has a comfortable,

cotton-like hand and appearance with stretch. Possible applications include sports and thermal

wear, intimate apparel, T-shirts, loungewear and others in which comfort stretch is desired.

Stretch-aire can be combined with other yarns for use in circular-knit and seamless styles.Accepta

yarns accept dye at lower temperatures than standard polyester, yet they still exhibit excellent

colorfastness and fade resistance, according to KoSa. They can be blended with other heat-sensitive

fibers such as spandex, wool and acetate to provide improved fabric performance and hand, styling

benefits and excellent printing and dyeing effects.Sample garments and fabrics made with Imbue,

Stretch-aire and Accepta may be viewed at KoSas fabric library in Charlotte.

October 2001

Welker Presents Condimat Conditioning Machine

Ph Welker GmbH, Germany, has introduced the new Condimat conditioning machine series.The Condimat

is based on a cylindrical autoclave body that can be manufactured with diameters of 1.6 to 3.0

millimeters (mm) and lengths of 1.5 to 14.0 mm.The Welker injector technology system injects cold,

saturated steam into the autoclave after five minutes, shortening the conditioning process to 35 to

45 minutes. According to Welker, the process can reduce energy costs up to 50 percent per kilogram

(kg) of conditioned yarn.Features of the Condimat include a new water-jet device to increase the

net moisture result; fully automatic packaging, wrapping or ticketing solutions; and a 10-year

autoclave guarantee for the autoclave vessels.

October 2001