Burlington ReorganizationBrings ChangesAs part of Burlington Industries Inc.s reorganization under

Chapter 11 of the U.S. Bankruptcy Code, the Greensboro, N.C.-based company has sold its residential

upholstery business and its bath consumer products assets.Bacova Guild Ltd., High Point, N.C., a

subsidiary of Ronile Inc., has acquired Burlingtons bath consumer products assets. The new business

will operate as a division of Bacova, and will sell under the Bacova® Bath and other brand

names.Tietex International Ltd., Spartanburg, has purchased Burlingtons residential upholstery

fabric business. The acquisition includes Burlingtons Sheffield facility in Rocky Mount, N.C.

Tietex expects to employ the majority of Sheffield employees.Tietex also plans to lease a portion

of the weave capacity at Burlingtons Williamsburg plant in Matkins, N.C. Employees associated with

upholstery production will be employed by Tietex.Tietex will use the Burlington House® brand name

for upholstery fabrics.Springs Industries Inc., Fort Mill, S.C., has completed its acquisition of

Burlingtons window treatments and bedding consumer products business (See Textile World News, April

2002). The purchase includes a manufacturing plant in Mexico. Springs also has received a license

to use the Burlington House® and American Lifestyle® brand names. In addition, Burlington will

supply finished products manufactured at its Reidsville and Stokesdale, N.C., facilities, as well

as fabrics to be converted by Springs into finished products.

July 2002

Burlington Reorganization Brings Changes

Fong39 S Launches Ecotech Dyeing Machine

Fong’s LaunchesEcotech Dyeing MachineFongs recently added the ECO-6 high-temperature dyeing machine to its Ecotech series of machines. The ECO-8 and ECO-38 were introduced at ITMA Asia in October 2001.The ECO-6 unit features the Multi-Saving Rinsing system (MSR); Multi-Intelligent Rinsing system (MIR); direct steam heating device for hot water filling; and an advanced, modulated dosing system. Maximum fabric speed is 350 meters per minute. The machine has a capacity of 250 kilograms of fabric per tube.July 2002

Apparel Sourcing Show Well Attended

Apparel Sourcing Show Well AttendedA total of 4,130 attendees from 1,253 companies visited 220 booths representing 162 companies and 22 associations during the 11th annual Apparel Sourcing Show, held in May in Guatemala City, Guatemala. The exhibition, organized by the Guatemala-based VESTEX commission, showcased Caribbean Basin (CBI) apparel and textile manufacturers, as well as presenting technology and machinery providers, seminars and conferences. The shows Matchmaking meeting program arranged more than 390 meetings between CBI apparel producers and U.S. and Canadian customers seeking manufacturing or sourcing alternatives.DuPont, Cotton Council International and Unifi launched a CBI sourcing promotional campaign during the show. The Apparel Sourcing Show has served us well as a means of informing the industry of our commitment to bring value to all participants in the apparel producing chain, said David Blondino, regional sourcing manager, DuPont TextilesandInteriors (DTI), Wilmington, Del. We are supportive of VESTEXs efforts to come up with new ways to facilitate relationships and generate business growth in the region. July 2002

Springs Nominated As Star Site

Springs Nominated As Star SiteSprings Industries window fashion facilities in Montgomery, Pa., have

been nominated as a Star Site under the Voluntary Protection Program (VPP), administered by the

U.S. Department of Labors Occupational Safety and Health Administration (OSHA).The program awards

facilities that monitor, measure and improve workplace safety. Out of 7 million worksites

nationwide, only 850 have qualified as VPP sites; Star Sites have about half as many injuries as

their industry counterparts.

July 2002

PGI Accesses DIP Facility

PGI Accesses DIP FacilityPolymer Group Inc. (PGI), North Charleston, S.C., and 20 of its U.S.

subsidiaries have filed for pre-negotiated reorganization under Chapter 11 of the U.S. Bankruptcy

Code.PGIs international operations and joint ventures are excluded from the filing.With the backing

of its bank group and the holder of more than two-thirds of its outstanding bonds, PGI hopes to

eliminate more than $550 million of debt. The company expects to complete reorganization by the

third quarter 2002.We expect that the restructuring process will generally have no impact on the

companys ability to fulfill its obligations to its customers and employees, said Jerry Zucker,

chairman, president and CEO. We fully expect that our vendors and customers will support the steps

taken today as part of our program to adjust our capital structure and strengthen the companys

position for the future.As part of the filing, PGI has received approval from the U.S. Bankruptcy

Court to access a $125 million debtor-in-possession (DIP) facility, arranged by JP Morgan Chase,

which will be used to fund operating expenses and to meet employee and supplier obligations.The

company already has received court approval to continue to pay employee wages and benefits, to pay

suppliers for delivery of goods and services, and to continue ordinary customer programs and

practices.

July 2002

BASF Adds Zeftron 200 To Recylcing Program Builds New Plants

BASF Adds Zefrton 200To Recycling Program, Builds New PlantsBASF Corp., Mount Olive, N.J., has expanded its 6ix Again® nylon recycling program to include Zeftron® 200 upholstery yarns.Upholstery fabrics made with Zeftron 200 nylon will be recycled in a similar manner as carpets returned through the 6ix Again program, now in its eighth year of evolution, said Tim Blount, manager, marketing programs. The nylon fiber will be recovered and then recycled back into virgin quality nylon 6 polymer at BASFs depolymerization plant in Arnprior, Canada.In other company news, BASF is developing an integrated production facility at the Shanghai Chemical Industry Park in China. The facility will convert butane into 80,000 tons of tetrahydrofuran (THF) annually, which will then be converted into 60,000 metric tons of polytetrahydrofuran (PolyTHF®). The plants are expected to come on-line in 2004 and will supply Chinas spandex fibers market. July 2002

Unifi Opens Hong Kong Sales And Marketing Entity

Unifi Opens Hong KongSales And Marketing EntityGreensboro, N.C.-based Unifi Inc. has formed a new sales and marketing subsidiary in Hong Kong. Unifi Asia Ltd. will allow the company to better serve its worldwide customer base and to take advantage of future growth opportunities existing in the region. Asia is a strategic area of focus for the company, said Mike Delaney, senior vice president, Unifi.July 2002

Kellwood Initiates Gerber Offer To Supply Casual Male

Kellwood InitiatesGerber Offer, To Supply Casual MaleSt. Louis-based Kellwood Co. is proceeding with plans to acquire Greenville, S.C.-based Gerber Childrenswear Inc. Kellwood subsidiary Cradle Inc. has commenced an offer to exchange any and all outstanding shares of Gerber common stock for cash and Kellwood common stock. In addition to marketing infant and toddler apparel and related products, Gerber Childrenswear owns Auburn Hosiery Mills Inc., Auburn, Ky., and Sport Socks Co. Ltd., Ireland.Edward Kittredge, chairman, president and CEO of Gerber Childrenswear, will continue to head the company, reporting to Robert C. Skinner, corporate vice president of Kellwood.In other news, Kellwood has signed a contract to supply mens sportswear, activewear and furnishings to Designs Inc., new owner of Casual Male Corp. Total purchases over the seven-year term should exceed $400 million, with first shipments targeted for Spring 2003.July 2002

Charles A Hayes Dies At Age 68

Charles A. (Chuck) Hayes, chairman of Guilford Mills, Greensboro, N.C., and president of the

American Textile Manufacturers Institute (ATMI), Washington, for the 2001-2002 term, died Sunday,

July 22 in Myrtle Beach, S.C. He was 68.Hayes turned the one-plant Guilford operation into a

dominant force in the textile industry during his tenure as CEO from 1971-1999. The company earned

a spot on the Fortune 500 in 1988.As the first knitter in the ATMIs history to be elected

president, Hayes sought to bring a united front to the organization, giving all sectors of the

textile industry a unified voice.In addition to his professional accomplishments, Hayes was also a

philanthropist, donating time and money to literacy causes. Hayes served on the University of North

Carolina – Greensboro Board of Trustees from 1980-1991, serving as chairman for six years. He

pledged $666,666 to the school to endow a professorship at the School of Education.

Import Problems Persist

I

nternational trade concerns — both short-term and over the longer pull — continue to

plague mills. Looking at the current year’s outlook first, all signs point to an increase in

incoming shipments — reversing the small, recession-induced slippage noted last year.

To be sure, there are some restraints that will limit any advance, including: the lobbying

efforts of the new American Textile Trade Action Coalition (ATTAC); and expectations of a somewhat

weaker dollar, which could soon make imports more costly. Nevertheless, improving U.S. consumer’s

demand should outweigh these positives and make some import gain inevitable.

How much gain? At this point in time, our projections suggest about a 3- to 5- percent

textile and apparel increase on a square meters equivalent (sme) basis. Not good, but a lot better

than the steady tattoo of double digit advances that prevailed as recently as 2000.

China: A Long-Range Question Mark

But of even bigger concern is the question of what happens in early 2005, when virtually all

quotas are eliminated for World Trade Organization (WTO) countries.

One fear is that China (already the top and fastest growing exporter to the United States)

will at that time become an even more potent competitor of low-cost, high-quality textiles and

apparel.

Point to keep in mind: China’s expertise and manufacturing sophistication already equals or

even tops that of other exporters in both Latin America and the Far East. Upshot: More big changes

in trade flows are inevitable.

Some Indications Of A Turnaround

On a somewhat more optimistic note, there’s a growing consensus that recent declines in

domestic mill output are over. The feeling is that totals are likely to hold near current levels

for the next few years.

Indeed, there are already signs of some bottoming out. Textile purchasing executives now say

they are experiencing increases in both new orders and shipments. Equally significant is the jump

in the textile mill workweek — from 40.3 hours a year ago to 42.1 currently. And, as pointed out in

previous columns, the textile inventory glut continues to fall significantly — making it

increasingly likely that new orders will be quickly translated into new production.

Zero in on individual fabrics, and the picture is also looking somewhat brighter. Thus

denim, after a very poor second half in 2001, is again moving well — helped by a growing number of

new fabric finishes. Khaki is also making a comeback with novelty looks, better quality and new

stain-resistant qualities. Dress shirt fabrics are perking up, too — as the trend toward “dressing

up” intensifies.

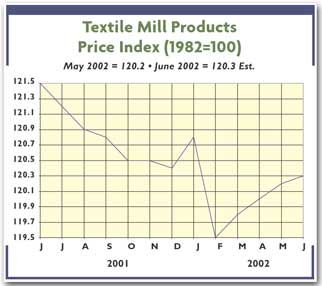

More Thoughts On Costs

A new DRI-WEFA study on costs also has to be regarded as quite encouraging. The big

econometric consulting firm, taking a look at the textile mill industry, finds that input costs

(including both services and materials) is now lagging year-ago levels by a percentage point or

two.

Much of this is due to the very modest labor hikes, which are now more than being offset by

productivity gains. And the picture is much the same for materials where cotton weakness has more

than compensated for some recent pickup in polyester quotes.

Moreover, all this good news is projected to continue. To be sure, the DRI-WEFA study does

see an end to cost declines.

On the other hand, its new forecast is still basically upbeat — calling for only about a

1-percent-or-so annual increase in material and service costs over the next year and a half.

A Closer Look At Overall Demand

A slowly strengthening economy would also seem to bode well for the industry. Current

consensus calls for about 3-percent GDP growth at the annual rate over the next few quarters.

This, in turn, should help make for similar rises in consumer incomes and spending levels.

Aiding gains will be such additional fillips as little or no price inflation, continuing low

interest rates, and a still-booming housing market. The latter not only is feeding demand for home

furnishings, but is also allowing homeowners to tap into home equity for spending.

Lastly, this robust home market is keeping household net worth at or near peak levels

despite a still-weak stock market.

Factor these pluses into the textile equation, and it may well explain some of the cautious

optimism being voiced by industry analysts and executives.

July 2002