Jentex Develops JENBondAdhesive Web ProductsJentex Corp., Buford, Ga., has developed JENBond Adhesive Web products to provide increased production efficiencies and reduced environmental impact in laminating processes. Jentex can produce web and composite roll goods in widths up to 64 inches. Matt Pelham, president, said Jentex has worked to produce adhesive web products that are competitive with other products in the marketplace, but also to offer additional products with lower melt points and high bond strengths to cover a wide range of applications. Our product trials have been successful and our customers are satisfied, said Pelham. We are now making the investment to take these products [JENBond] to market.June 2002

Shelton CTI Develop Elastane Relaxation System

Shelton, CTI DevelopElastane Relaxation SystemCollaboration between Shelton Machines Ltd. and CTI, both based in the United Kingdom, has resulted in a new on-line relaxation system for elastane fabrics. The Shelton C-Tex Fabric Relaxation system allows consistent finished length and width measurement of elastic fabrics during processing. The system was developed in response to the desire of Textured Jersey, a British manufacturer of fabrics containing elastane, to supply completely relaxed fabric to its customers. It combines on-line inspection and CTIs C-Tex relaxation® technique of air flotation fabric relaxation in a single machine. Textured Jersey has purchased several of the machines. Shelton and CTI have applied jointly for a worldwide patent for the technology.July 2002

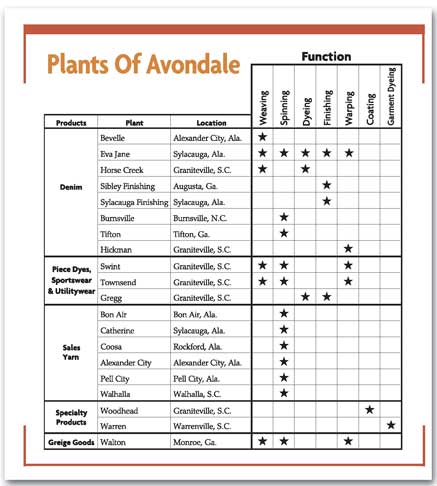

Investments That Work

Investments That Work

Avondale Mills’ ongoing capital investment plan positions the company for low-cost delivery and

high-quality production. With a rich history of investment, acquisition, and focus on

quality, Avondale Mills is no stranger to innovation. A closer look at the companys technical

history reveals a well-honed strategy of plant and equipment upgrades, always positioning the

company for low-cost delivery of high-quality products.Since the acquisition of the Graniteville

Company in 1996, Avondale has invested more than $300 million in capital equipment. In 2000 alone,

more than $115 million was invested by this privately held firm. How does a private firm with

more than 5,600 associates, 20 plants and sales in excess of $600 million stay on course In

Avondale Mills Chairman G. Stephen Felkers words: More than 100 years ago, the visionaries who

formed Monroe Cotton Mills incorporated into their creed some fundamental precepts of doing

business, goals that we adhere to today.

Avondale’s Gregg Finishing Plant uses the latest computer technology to monitor its dye and

resin ranges. According to Felker, these fundamental precepts include:producing a product that

meets the needs of customers;ensuring a safe working environment for associates;taking pride in

manufacturing quality products;delivering on time; andpaying scrupulous attention to costs so that

a reasonable profit can be made.Weve made investments in good times and bad. Our dedication to

keeping Avondale modern and competitive is absolute, Felker continued. By reinvesting in Avondale,

weve equipped ourselves with the tools to fight not only domestic competitors, but imports from

low-wage countries as well.With an ongoing capital investment plan and plants that span spinning,

weaving, dyeing and finishing, Avondale Mills offered

Textile World a peek inside some of its most recent plant modernization

projects. Horse Creek PlantThe Horse Creek Plant, Graniteville, S.C., is a sound example from

Avondales acquisition and modernization history

(See Full Steam Ahead, TI, May 2001). As part of the 1996 Graniteville purchase, the plant

became the focus for consolidating Granitevilles weaving from other facilities, as well as a

platform for continued expansion as a world-class denim operation.With help from Suitt

Construction, additional space was added to make room for 240 Picanol Omni air-jet weaving

machines. These machines are fed by two computer-integrated Morrison indigo warp-dyeing ranges and

18 beaming machines, the most recent purchased from McCoy-Ellison. Hubtex beam-handling equipment

facilitates moving product, while West Point FoundryandMachine Co. provided four

computer-controlled slashers that deliver high-quality warps to the weave room.

With quality at the heart of the weaving operation, the Picanol Omnis feature Alexander

Machinerys (ALEXCO) off-loom take-ups. As well, four Ingersoll-Rand air compressors were essential

additions to the air-jet installation. Pneumafils filtration systems and Luwa Bahnson/Parks Cramer

traveling cleaner systems ensure the proper weaving environment.Horse Creek was the first new

facility built by Avondale in some time. According to the company, the project was on a tight

timeline, but the efforts of Suitt Construction, Pneumafil, Picanol and the Avondale Engineering

Group kept the project on schedule so that it finished on time and within budget.It was an amazing

process to see the bare ground become a modern weaving mill in a matter of months, said Tim

Stansell, vice president, Manufacturing Services. Coosa’s Linked UpgradesAvondale Mills Coosa

Plant, Rockford, Ala., is the companys first linked spinning operation. Specializing in carded

yarns for its sales yarn business and weaving operations, Coosa features Crosrol bale opening and

cleaning equipment, which leads to eight new Marzoli roving frames and 23 Marzoli ring-spinning

frames. Schlafhorst placed 12 winders, and most recently, seven Savio Orion I winders have been

added. Filtration systems by Roy L. Hartness keep Coosas environment contamination-free.Mark

Tapley, executive vice president, Western Operations, said, The upgrade at Coosa spearheaded our

entry into linked ring yarn production. The improvements we realized in quality and costs

buttressed our effort to be the leader in the yarn markets. They also not only reinforced our

determination to expand in carded yarns, but also convinced us to proceed with a linked yarn

approach in combed cotton sales yarns. Alexander City

May 2000 brought the announcement that Avondale would invest $32 million in the conversion of

a portion of Bevelle Plant, Alexander City, Ala., to form Alexander City Plant. Bevelle continues

to produce high-quality denim fabrics, and the newly minted Alexander City Plant has been

fine-tuned to produce combed cotton yarns for the knitted apparel industry.Rieter, Marzoli and

Savio are at the center of the investment. There are two Rieter opening lines and 24 Rieter C51

cards with integrated grinding and Advanced Blowroom Control (ABC). Tateishi sliver cans feed eight

Rieter SB-D 10 drawframes for pre-drawing, monitored by Rieters SPIDER web system.Twenty Rieter E72

combers and eight RSB-D 30 finish draw frames with sliver guard utilize the UNIlap E32 transport

system to feed eight Marzoli FT 1-D roving frames with auto doffing. A roving transport system from

U.T.I.T. delivers roving to 25 Marzoli RST 1 ring-spinning frames that have a total of 32,400

spindles. Auto creeling of roving, automatic bobbin doffing and linked winding maximize

efficiencies. Savio winding systems take the form of 12 30-position and 13 38-position Orion I

winders with Uster Quantum Clearers to maximize yarn and package quality. The Orion I winders with

twin splicing produce quality yarn packages with strong splices, said Tapley.The yarn we are able

to produce at Alexander City has defined a new level of quality in the combed-cotton sales yarn

market. The level of technology achieved at Alexander City is the highest that is available with

current machinery, said Wayne Spraggins, corporate vice president and president, Manufacturing

Operations. Swint And TownsendThe Swint and Townsend Plants, both in Graniteville, provide the

spinning and weaving operations for Avondales sportswear and utilitywear fabrics. New machinery

complements and adds value to existing equipment that was kept after recent upgrades at the

plants.Swint, after a two-phase construction project, now weaves sportswear and utilitywear fabrics

using 110 Picanol Omni air-jets and 72 Omni Plus air-jets, in addition to the existing 101 Nissan

weaving machines. Townsends 80 Picanol Omnis round out the plants loom installation, which includes

49 Tsudakomas and 47 Nissans. Todo warp-tying equipment is used in both locations.Townsend houses a

new, modern linked ring spinning department, which includes nine Zinser roving frames, 27 Zinser

ring-spinning frames and 27 Schlafhorst winders. The department makes yarns ranging from 6/1 to

20/1 in size and, according to Avondale, the increased capacity is producing a stronger yarn for

optimum weaving performance.The capital investments at Swint and Townsend have enabled them to make

a better product at a lower cost, said Bo Bonner, executive vice president, Eastern Operations. In

fact, half the spinning production from Townsend is used to supplement the increased weaving

capacity at Swint. From start to finish, these mills are making a better-quality yarn, which, in

turn, makes a higher-quality fabric, Bonner added. Gregg Plant: Reinvestment In FinishingOur

investment in Gregg Plant supports our strategy of building a piece-dye, sportswear and utilitywear

unit in Graniteville. Swint, Townsend and Gregg Plants give us the flexibility and quality we need

to succeed in todays marketplace, explained Keith Hull, corporate vice president and president,

Marketing and Sales.Greggs modernization represents more than $30 million in Avondale reinvestment.

Central to the operation is a new 300-foot-long, high-speed dye range from Kusters that was

installed in 1998. The range features full monitoring and control by ABB, and dyes fabric at the

rate of 150 yards per minute.With a wash range and sanforizers supplied by Morrison Textile

Machinery, the finishing operation is rounded out with six sueders from Lafer. Despite Greggs huge

capacity, a wide array of finishes and surface treatments, and an infinite color spectrum are

available to our customers. Flexibility is a requirement of a full-service company like Avondale,

said Tony Royster, vice president, Dyeing.Krantz inspection tables and 10 EVS fabric-inspection

systems provide the tools necessary to ensure that quality is delivered in every yard. To earn the

large orders necessary to sustain the high volumes demanded by an operation such as Gregg, we must

deliver quality greater than that of our competitors, and deliver it on time, Hull said. The

knowledge of this requirement drives our management approach to machinery selection, plant

staffing, scheduling and quality control. Consider The WholePlant modernization and equipment

selection is just part of the story at Avondale. Talented and motivated associates make our

investments work; without qualification, these people are Avondales greatest asset, said Felker. We

rely on our machinery suppliers to provide us with leading-edge technology. As it evolves, we will

embrace this technology to enhance our competitiveness in terms of quality, cost and customer

service. It is not enough simply to buy new machinery; investment in technology must be justified

by improvements that are realized in the workplace and in our product and service. We will continue

to make every effort to ensure not only that we have the finest technology, but also obtain the

benefit from it.With a successful track record of more than 150 years, it would be easy for

Avondale to become trapped by the weight of its own history. On the contrary, Avondale Mills builds

on the past with a strong sense of its customers needs and its committed associates, seemingly

always ready to invest strategically to remain competitive and stay on course.

June 2002

DuPont TextilesandInteriors To Reduce Global Workforce

DuPont TextilesandInteriors ToReduce Global WorkforceIn an effort to become a more competitive,

integrated organization, DuPont TextilesandInteriors (DTI) plans to reduce its global workforce by

more than 2,000 employees. Ten percent of Wilmington, Del.-based DTIs workforce will be terminated,

with more than two-thirds in manufacturing facilities and offices in the United States, and the

rest in Europe.DTI has manufacturing facilities in 50 countries, with an annual revenue of $6.5

billion, and, according to the company is the worlds largest integrated textile fiber and interiors

business.These are difficult but necessary actions to position DTI for success in a highly

competitive and rapidly consolidating industry, said Richard R. Goodmanson, executive vice

president and COO.We must act quickly and decisively to match our resources with current market

realities. We are committed to doing what it takes to capture market opportunities while serving

our customers with speed and flexibility, he said.More than half of the affected employees will

leave DuPont by July 31.As part of the restructuring, the Terathane® PTMEG manufacturing plant in

Niagara Falls, N.Y., and less competitive portions of spandex operations in Waynesboro, Va., will

be closed.DuPont expects to achieve annual pre-tax cost savings nearing $120 million as a result of

these restructurings realizing 30 percent in 2002 and 100 percent in 2003. The company expects to

take a one-time second-quarter charge of 12 to 16 cents per share. The company projects two-thirds

will be attributed to employee separation costs and one-third to asset shutdowns. The actual

one-time charge to earnings will be available at the end of the second quarter 2002.

June 2002

Future Focus

ACIMIT

Textile World Special Report Future Focus

ACIMIT targets developing markets to ensure growth in 2002. T he Italian textile

machinery sector, represented by the Milan-based Italian Association of Textile Machinery Producers

(ACIMIT), experienced limited production and export growth in 2001. Sector trends were affected

last year by economic downturns such as those in the United States and the European Union (EU),

according to ACIMIT. Other important markets, such as Turkey, also were hit hard. Last year

experienced only a 5-percent growth in both production and exports over 2000 levels.

The most requested Italian textile machines in 2001 were spinning machines, which

accounted for 25 percent of all textile machinery. Finishing machines represented 24 percent, and

weaving machines accounted for 22 percent.The current year is showing signs of recovery, leading to

expectations of more sustained growth than was seen in 2001. This could be due to the parallel

recovery of international economies such as those of the United States and the EU.In an effort to

ensure that 2002 is a year of growth and profit, Italian textile machinery producers are continuing

to focus on Asia. ACIMIT already has launched a Chinese version of its website in an effort to aid

Italian companies in reaching this important market. Other developing markets, such as Eastern

Europe and Central America, also are areas of focus. The North American and other European markets

also will receive attention.ACIMIT plans to collaborate in 2002 with the Italian Institute of

Foreign Trade (ICE) in an effort to support internationalization activities within its member

companies.Other ACIMIT initiatives for 2002 include involvement in sector trade fairs, including

CITME in Beijing and Saigontex in Saigon. Technological seminars in Central America and North

Africa, as well as training courses for textile operators in Italy and abroad, also will take

place.

June 2002

3M Uncovers Fraud Offers New Thinsulate Products

3M Uncovers Fraud,Offers New Thinsulate ProductsThrough its Product Authenticity and Selection System (P.A.S.S.), designed to address the issue of brand counterfeiting, St. Paul, Minn.-based 3M recently uncovered fraudulent use of its Thinsulate brand name on hang tags describing insulation used in a line of fingerless gloves. 3M worked with the manufacturer to identify the fraud. All the gloves were removed from the market and destroyed.In other news, 3M has introduced two new Thinsulate products. Thinsulate supreme insulation contains a special fiber coating that adds a luxurious, silky softness and drapability to Thinsulates breathability, moisture resistance, durability, warmth and comfort, according to 3M. It also is machine-washable and -dryable. Thinsulate insulation type g provides the standard Thinsulate attributes and is priced to compete with other low-cost insulation products.June 2002

Amendments To Flammability Act Introduced

Amendments ToFlammability Act IntroducedA movement is underway in Congress to amend and expand coverage of childrens sleepwear regulations under the Flammable Fabrics Act. Senators John Breaux (D-La.), Hillary Rodham Clinton (D-N.Y.) and Joseph Biden ( D-Del.) have each introduced legislation that would reverse a Consumer Product Safety Commission regulation that exempted childrens sleepwear sizes 0 to 9 months and tight-fitting sleepwear from the flammability regulations. In issuing the revised regulation, the commission said infants are not mobile and therefore are not at risk, and that tight-fitting garments will not support flames.The three bills would reverse that decision, but the Breaux bill goes much further than the other two. It not only would restore coverage of infants and tight-fitting garments, but also would extend coverage to what Breaux calls a functional definition of sleepwear for children up to seven years of age. That definition would include any garments that are sometimes used as sleepwear, such as togs, bunny suits and garments with cartoon characters that are attractive to young children.June 2002

Commitment To Quality

Commitment To Quality From Avondales various beginnings more than a century ago to the

present, a commitment to quality has guided the company. Quality is achieved by using the finest

raw materials, machinery and equipment, and keeps customer satisfaction at a high level.Early on,

the company involved its associates in a proactive implementation of quality assurance. The Zero

Defects Program, introduced in 1966, encouraged the associates to suggest ways to improve quality,

safety, customer service, maintenance and efficiency.Quality control is vital as Avondale

modernizes operations in each of its mills. Keeping up with the latest developments in

quality-monitoring technology, the company is using state-of-the-art equipment in every phase of

its manufacturing processes. 24/7 On-Line MonitoringRecent upgrades at Alexander City, Coosa

and Pell City include the latest Uster quality-monitoring software and equipment to provide a

comprehensive real time picture of the entire operation. Twenty-four hour quality monitoring allows

us to know what goes on at all points of yarn manufacturing, said Josh Morton, quality assurance

manager, Alexander City Yarns. Whereas before we were checking random samples daily, now we are

able to check samples every second of the day. At Alexander City, Usters Sliver Expert

monitors the carding process. Ring Expert, installed on the spinning frames to monitor production

and efficiency, records the number of ends down and pounds produced. Cone Expert and Quantum

Clearer at each winding position ensure final yarn package quality, detecting and cutting out

foreign matter, unevenness or hairiness in the yarn prior to winding.Finally, physical testing in

the lab is accomplished using Usters Lab Expert. The system includes UT4 to test for evenness,

Tenso Jet to test for strength and elongation, and the AFIS fiber information system.

At Alexander City, 12 30-position and 13 38-position Savio Orion 1 winders accomodate various

yarn counts. The Cone Expert system examines every winding position with Quantum Clearer monitoring

devices to ensure the highest quality. Coosa Plant also is using the Ring Expert and Cone

Expert systems, and Pell City is using Cone Expert in its winding operation.Usters Rotor Expert

system is installed at Tifton. Walhalla and Burnsville have added newquality-monitoring technology

to existing equipment. Improved monitoring in Avondales spinning operations helps detect

misperforming spindles and rotors and correct all problems before shipping of the final product. As

the company quips, One bad rotor can make a lot of bad yarn.Avondale says improved yarn quality has

led to dramatic improvements in fabric quality. Investments in greige mill quality have brought

point counts to an all-time low, and improved yarn strength has helped bring weaving efficiencies

to the highest levels ever.Investments at Gregg Plant are yielding consistently higher volumes of

first-quality fabric. Bigger barrels on A frames have reduced creases. Dye ranges are equipped to

reduce the amount of lint, thereby reducing spots on finished fabric. In the cloth room, cameras

mounted on machinery film every inch of fabric for on-line viewing and assignment of point

values.As Avondale pursues its commitment to invest in the most advanced machinery and equipment to

ensure quality in the manufacturing process, it is honing its competitive edge to succeed into the

next century and beyond.

June 2002

The Light Is Shining Brighter

A

ll spinning systems are running full and across most counts. One spinner said, “Ring

spinning is really going great. Open-end is also running pretty good, but demand is not as strong

as for ring-spun yarns.

Air-jet spinning is also much improved.” However, he went on to say, “With all of this good

news about running and operating at capacity, prices are still depressed. Retailers continue to

keep the squeeze on, pressing for that last penny — and that has driven the entire margin out of

the system for us. We are barely covering variable cost, and you know that we can’t survive like

this in the long run. Running flat out doesn’t always get it. We have to have margins. At some

point, we have to find a way to make some profit.”

There have been statements about restocking the pipeline and inventory when the economy

turns upward.

A spinner said, “What we are producing right now is going directly into the pipeline — none

of it is for inventory. And from what I hear, others that are running pretty good are producing to

satisfy orders. Not many are producing anything for inventory. Some are buying to help them meet

their commitment.”

“Things are getting much better,” responded another spinner. “Most are running at capacity,

six or seven days a week. Some plants that were in deep trouble a few months back have found new

life, and they are running full. Maybe the economic turn will be enough for them to survive for the

time being and really make it in the long run.”

Raw Material Prices Remain Low

Demand for U.S. cotton continues to be weak. Quotation for the base grade in the seven

designated markets averaged 29.43 cents per pound. This weekly average was down from 30.98 cents

per pound for the previous week and 47.22 cents for the corresponding week a year ago.

Most indications are that cotton prices will remain relatively low. There are high global

inventories, and domestic carryover was high. The farm bill that is in the works will give cotton

producers some relief and should further increase supply. Domestic consumption probably will not be

much different from last year.

The U. S. Department of Agriculture (USDA) estimates domestic consumption of 7.8 million

bales, up slightly from last year.

An interesting note: At a recent meeting of several textile manufacturers, one said, “There

is not enough spinning capacity in place in the U.S. to consume what the USDA has projected. The

USDA has projected a 7.8 million-bale consumption for the 2002/2003-crop year. The reason is

simple. There was a significant loss in spinning capacity last year. With this loss in capacity,

there is no way to consume that much cotton — even with all of the current mills running flat out.”

Some are saying we might be lucky if domestic consumption reaches just under 7 million

bales. Let’s hope consumption reaches 8 million. This would mean several plants would have to be

brought back on-line and consume a lot of cotton.

Domestic Versus Importer Products

One spinner said, “Have you ever heard that cotton ain’t cotton or yarn ain’t yarn or fabric

ain’t fabric?” He went on to say, “If you take a product from the shelf of a Wal-Mart/Kmart-type

store today and compare it to a product from the same shelf ten years ago, you will find that it is

probably a different product. In all probability, it is not the same cotton, yarn, fabric — or

perhaps there are small differences in construction. These are differences, maybe very subtle, that

the final consumer doesn’t see or isn’t even aware of. And if they aren’t aware or don’t know, then

this is a valid reason for not caring.”

This not knowing might be more of the reason that consumers “just” focus on prices. Some

might argue that if consumers were really aware and had an understanding of these differences in

product quality and performance, they might be more willing to spend an extra buck for the

difference.

Maybe it is an educational process. Letting the consumer know and understand that products

made in the United States are different from those substitute products that are imported is very

important. If they are not different in the consumer’s mind, we know what will happen. If they

really are not different in some way, then we have to make them different or go out of business.

June 2002

Getting It Right The First Time

By Gary N. Mock, Ph.D., Technical Editor Getting It Right The First TimeImproved dyes, processes ensure cost-effective, high-quality dyeing. There is a battle of titanic proportions taking place in the fiber world. Will it be polyester or cotton that emerges as the most-used textile fiber around the world Polyester has steadily increased its share of the world market and is expected to replace cotton as the leading textile fiber sometime in 2002. Industry sources predict that some 18 million tons of each will be used in the textile market far more than nylon, the nearest competitor. It is not surprising that leading dye manufacturers have concentrated their research and marketing efforts on dyes for these two traditional fibers. New Fiber-Reactive Dyes For Cellulosic FibersSwitzerland-based Ciba Specialty Chemicals now has three complete dye ranges for fiber-reactive exhaust dyeing: the Cibacron® FN range for warm dyeing; the Cibacron LS range, which reduces the amount of salt needed in dyeing; and the Cibacron H range for hot dyeing. New products include dyes for black formulations that offer versatility and more economy: Cibacron Black LS-N-01hc and Black W-US. The first is 10 percent stronger than the previous LS-N high-concentration and also is suitable for one-bath polyester/cellulosic dyeing in the LS Superfast process.Black W-US has outstanding build-up, and very good washing-off and wet-fastness; is dischargeable; and is available as a high-concentration formulation, according to Ciba. Also new are two greens that offer improved shade consistency and quality: Cibacron Green FN-BL and Green H-BL. New products in the H range include: Yellow H-G, Orange H-R and Red H-F.

Clariant AG, Switzerland, has nine dyes with outstanding fastness within the Drimarene HF range:Scarlet HF-3G; Blue HF-RL;Red HF-2B;Navy HF-G; Brown HF-2RL;Orange HF-2GL;Red HF-G;Yellow HF-R; andNavy HF-B. Each has a special function within the line. Scarlet HF-3G is the only one recommended for nylon as well as cotton. It is a very bright scarlet to be used as a straight color or in combination with Yellow HF-R, Orange HF-2GL and Red HF-2B for orange. Blue HF-RL is a reddish blue with good build-up and high lightfastness (co-complex), the company claims. It is best used in a ternary combination with Yellow HF-R or Orange HF-2GL and Red HF-G or Red HF-2B or Brown HF-2RL. Red HF-2B is a bluish red for use in a ternary combination with Yellow HF-R or Orange HF-2GL and Blue HF-RL or Navy HF-B. Navy HF-G is a slightly greenish navy with moderate lightfastness. It can be used as a straight color or in a ternary combination for medium to dark shades with Yellow HF-R or Orange HF-2GL and Red HF-G or Red HF-2B. Brown HF2RL is a neutral, homogeneous brown for use in a lightfast ternary combination with Orange HF-2GL and Blue HF-RL. Orange HF-2GL is a non-phototropic dye for use in a ternary combination for high lightfastness with Brown HF-2RL and Blue HF-RL.Red HF-G is a brick red. It can be used in an economical ternary combination with Yellow HF-R or Orange HF-2GL and Blue HF-RL or Navy HF-B. Yellow HF-R is a slightly reddish yellow for use in a ternary combination with Red HF-G or Red HF-2B, Blue HF-RL or Navy HF-B. New Disperse Dyes For Polyester

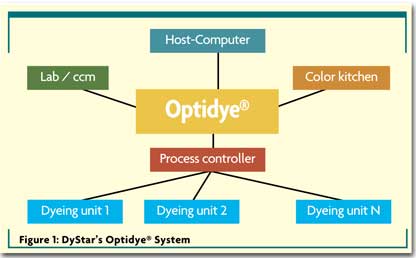

Ciba Specialty Chemicals offers a broad spectrum of dyes for various applications.Photograph courtesy of Ciba.Ciba also has introduced a new range of liquid disperse dyes for the automotive business. This Terasil range gives the exceptional lightfastness demanded by this industry, according to Ciba. Suitable for exhaust dyeing and printing, they include: Blue HL-B, LIQ. 75%;Pink 2GLA, LIQ. 50%;Blue BGE, LIQ. 50%; and Yellow GWL, LIQ. 50%. Germany-based DyStar recently announced a restructuring of the disperse line of dyes under the Dianix umbrella. According to Alan Cunningham, head of marketing of polyester dyes for DyStar, The new Dianix range has been designed to meet the changing needs of our customers for the coloration of polyester, who more than ever look for the highest levels of performance, quality and value to compete in the global market. The Dianix name was chosen because of its excellent name recognition throughout the world. DyStar was formed through the merger of the textile dyes businesses of Bayer AG with Hoechst AG in 1995. DyStar obtained the Dianix name from a previous agreement between Hoechst and Mitsubishi. The subsequent acquisition of the textile dyes businesses of BASF, Zeneca and Mitsui brought DyStar a large market basket of excellent disperse dyes, which now have been unified for different applications.Dianix CC dyes are a range of economical medium-energy dyes for rapid, reliable exhaust and continuous dyeing of polyester and blends with other fibers. With the use of computer control programs, the dyer can expect excellent Right-First-Time performance because these dyes are compatible. They also offer excellent build-up, economical dye recipes and good all-around colorfastness, according to DyStar. A scarlet, blue and turquoise are totally new.The Dianix XF/SF dyes are a range of dyes with the highest levels of washfastness. The dyer can expect little problem for high-washfast apparel, workwear and sportswear. DyStar claims the dyer will achieve high production efficiency, especially on polyester/cellulose blends, through alkaline clearing of unfixed dye, thereby eliminating the need for reduction clearing.The Dianix UN-SE dyes are compatible, level-dyeing dyes for reliable dyeing of medium and heavy shades on polyester fabrics. Once again, compatibility and computer control result in level dyeing performance on difficult fabrics, such as microfiber, and weight-reduced polyester.The Dianix AC-E dyes are three compatible, level-dyeing dyes for rapid, reliable dyeing of pale shades on polyester. Dianix PLUS is a new range of five compatible, level-dyeing dyes for reliable dyeing of medium and heavy shades, especially on microfiber and weight-reduced polyester, whether applied under mild alkaline conditions to control trimer, or under conventional acid conditions.The Dianix S line is an economical range of high-energy powder and liquid dyes with high fastness to contact heat. These dyes are used successfully in exhaust, continuous and printing applications.The Dianix Luminous/Brilliant line of dyes has been specially selected from the fluorescent and brilliant dyes for fashion shades and high-visibility work clothing. These selected dyes conform to the EN-471 specifications for high-visibility work clothing and the EN 1150 specifications for high-visibility leisure and sports clothing. Even with these difficult requirements, the colorfastness is still good.Dianix AM dyes offer the highest level of lightfastness for automotive and other demanding textiles. These dyes offer on-tone fading and minimum metamerism. There also is an alkaline dyeing option to avoid the problems of cyclic trimer deposition, especially noticeable in package dyeing and winding. A new red and a brilliant blue have been added to this line.Finally, the Dianix P dyes offer the dyer a complete range of economical liquid disperse dyes for textile printing. These dyes are suitable for standard applications as well as for specialties such as burn-outs, flags, banners and camouflage. Controlling Your CostsThere is no doubt in anyones mind that process control is the first step in controlling costs. Dyeing and getting it right the first time has significant cost advantages. With profit margins as thin as they are today, one simply must rely on ones system and believe that it is right. Of course, the control system has to be good. Over the years, DyStar has developed an advanced control system called Optidye. The system allows the dyer to link the process controller with the lab, host and color kitchen (See Figure 1). When individual machine characteristics and load size are factored in, there are bound to be slight corrections as one moves from one dye machine to the next. There are simply too many factors involved to keep track of this annually. Optidye has been proven in the field for years now.

Technodye – New Dyeing ProcessArgelich, Termes y Cia S.A. (ATYC), Spain, is working on an electrochemical dyeing process in close cooperation with the Catalonian Polytechnic University through the Instituto de Investigaciextil y Cooperacindustrial de Terrassa (INTEXTER), and with the support of Clariant. Such cooperation is devoted to developing a fabric-dyeing process using electrolytic dyestuff reduction specifically for sulfur, vat dyes and generally all dyes that require reduction. The trials already have been initiated in a computerized lab pilot machine installed at INTEXTER.The advantage of electrolytic reduction of dyestuff is that it avoids reducing chemicals, which in turn reduces contamination in the water, thereby eliminating 90 percent of the biological oxygen demand and chemical oxygen demand levels in the dyehouse effluent. The effluent is pure enough to be reused in subsequent dyeing. Trials have been concluded using black sulfur dyes on cotton knit fabric, with very satisfactory results.Textile World has tried to hit the highlights of some of the new developments in cotton and polyester dyes, along with controls and machinery that will make life easier for the dyer. Better dyes with better properties allow dyers to better satisfy their customers. New process technology can enable them to save money because fewer chemicals are used and less waste water needs to be treated. Lets have a greener world.June 2002