Textiles 2002

The worst is over, but recovery will be slow. Todays hard-pressed textile industry

coming off a miserable 2001 can probably look forward to some bottoming out, and even selective

fractional gains over the next few quarters. But by no stretch of the imagination does it look to

be anything even remotely resembling a good year.Blame it on the still-considerable number of mill

problems. Aside from the endemic headache, mills continue to face the multiple challenges of a

far-from-robust economy, excess capacity, a rapidly changing marketplace, fickle consumers and

relatively shaky financial positions.However, the situation is far from hopeless. Indeed, most

analysts see a viable domestic industry in the years immediately ahead one that may not be as large

as it once was, but one that will become relatively healthy, a lot more innovative, and

increasingly able to compete in what is now clearly a global market.To be sure, precise predictions

in these uncertain times are quite difficult to make. But at this stage of the game, heres a sketch

of what

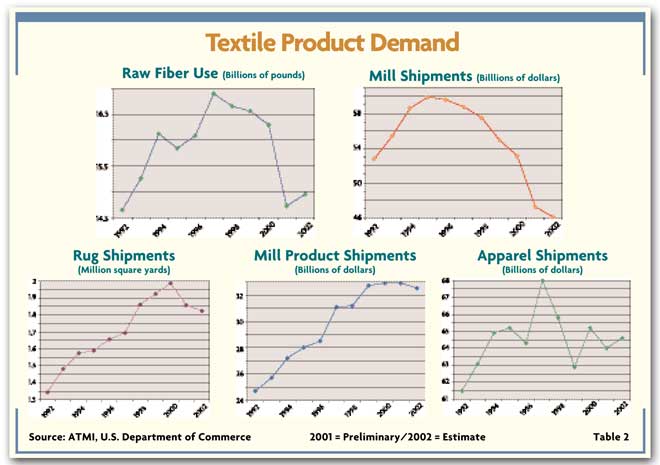

Textile World envisions for the upcoming year:Demand: Mill output for the year as a whole

will lag behind 2001, reflecting the steady declines of the past 12 months. But on a 2002

quarter-to-quarter basis, totals should remain relatively flat. A similar pattern is anticipated

for dollar shipments, with combined 2002 totals of both mill and mill products estimated at just

under $80 billion some $10 billion under the peak hit in 1997.Inventories: Expect some improvement

in the textile mill stock/sales ratio, as holdings are slowly brought down to match lower demand

levels. But little or no further declines are seen for the mill product ratios the needed inventory

correction occurred over the past year.Prices: The combination of lackluster demand, strong

competition, and more-than-ample capacity would seem to rule out any significant price advances.

There could be some small, selective increases, but not nearly enough to make for any meaningful

advances in any major mill or mill product price categories.Costs: This is the one saving grace a

potent offset to still-sluggish prices. Specifically, there will be only modest increases in labor

rates, and they will be offset by continuing productivity gains. Fiber costs will show little or no

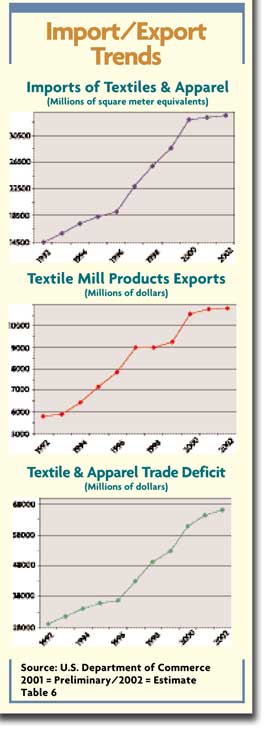

meaningful upward movement from current low levels.Foreign Trade: Import gains will be quite

modest, primarily because of the current domestic business slowdown. But because the economic

slowdown is now worldwide, it would be unrealistic to expect any export gains either. Look for

another huge textile and apparel deficit one that could top $65 billion for the first time in

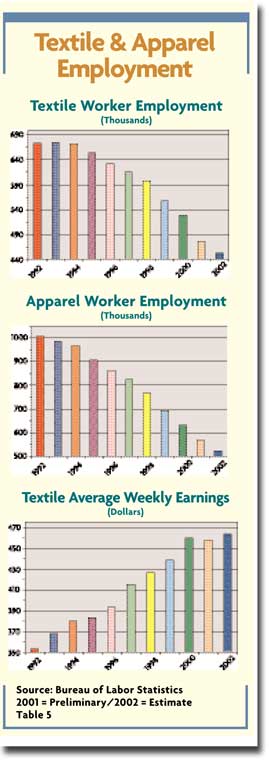

history.Employment: Industry shrinkage is best illustrated by the continuing decline in textile and

apparel employees. Add lessened demand to rising productivity, and the textile workforce should

drop another 5 percent to 453,000 over the new year. The apparel total could be off by 7 percent,

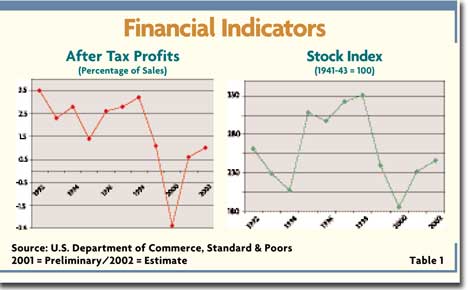

to around 529,000 workers.Financial: Profit margins will begin to inch up, but only from very low

2001 levels. Moreover, theyll remain well under the U.S. industry average. This, in turn, will

limit any stock market recovery from recent lows though some slight uptick in textile securities is

likely as the general economy begins to improve.Capital Spending: Purchases of new, more flexible

equipment will continue and help bolster the overall upward productivity trend. Nevertheless, the

total of such outlays should dip again in 2002 as industry activity continues to disappoint and

current capacity utilization remains in the disturbing low-70s range.New Products/New Processes:

The still-growing number of new offerings is one of the industrys long-term plusses. Details seem

to assure makers of apparel and other textile-containing products of a spate of new products. These

innovations also enhance the trend toward more product differentiation something that can give U.S.

producers a leg up on overseas competitors.Another sign that the industry isnt about to disappear

is the continuing wave of mill acquisitions, consolidations, mergers, reorganizations and global

partnerships all designed to assure a viable industry over the longer pull.Finally, its hard to

ignore all the trade legislation of the past few years. While this clearly presents lots of

challenges, it also provides plenty of opportunities for U.S. textile firms to increasingly become

suppliers of choice for North American and Caribbean manufacturers.Bottom line: dont write off the

textile industry. True, mill activity has nosedived nearly 20 percent over the past few years, and

this, in turn, has dropped the mill labor force to less than half the million-plus level prevailing

as recently as 1992.A recent longer-term forecast by the prestigious DRI-WEFA economic consulting

firm calls for a basically flat mill activity pattern over the next four years, with output

declining only fractionally over this period. In the latter half of the decade, these economic

pundits see a move back into the plus column, though any gains are likely to be quite

minimal.Recent long-term government textile employment predictions tell much the same story.

Workforce totals will continue to fall. But when increased productivity per worker is factored in,

the figures suggest level-to-slightly-higher mill production levels.

A Closer Look At 2002 MarketsAs noted earlier, overall mill production and shipment

totals over the new year arent likely to be rising much from recent levels. One big braking force

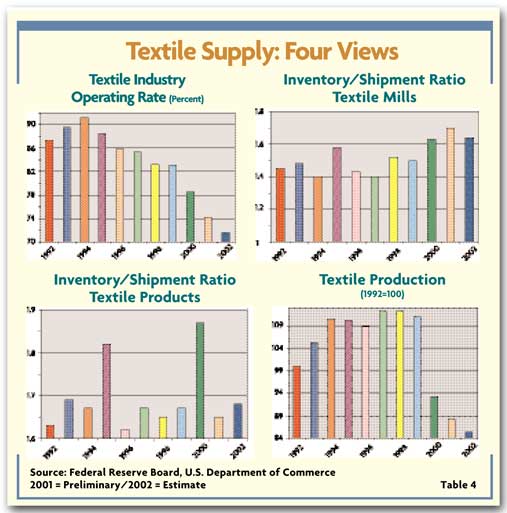

here will be the still-very-high mill inventory levels.The key textile mill/stock sales ratio now

near a 1.70 months supply is significantly above the 1.40 low in 1994. This very high ratio is

almost sure to have a negative effect on textile activity as a fair amount of early 2002 demand is

met by drawing down existing stocks rather than by new output. A relatively low mill operating rate

also doesnt bode too well for the industry. Right now, mills are operating at only 73 percent of

their potential a far cry from the 91-percent peak hit in 1994. Moreover, theres little to suggest

this key barometer will be turning up anytime soon.But not all areas of the industry will be

equally impacted by these problems. Denim markets, for one, look to remain tolerably firm, thanks

to a variety of new weaves and washes plus a still-growing interest in fashion constructions. Some

fleeces, velours and nylon types are also moving well. And corduroys, too, remain fairly

strong.Zeroing in on menswear, a fashion shift toward luxury and elegance should help both

wool/cashmeres and all wools. Biggest interest may be in light wools for pants. In coats,

wool/cashmere blends will dominate.The outlook for nonwovens is also fairly bright. And that goes

for the two segments of this fastest-growing textile area: the high-volume roll goods going into

diaper and feminine hygiene markets; and specialty markets for industrial applications.As well,

nonwovens are tending to make for new classes of products instead of replacing older markets. New

markets include allergen-barrier products, negatively charged dusting materials and vacuum filters,

and incontinence products for an aging population. But at the other end of the spectrum are several

weak spots. Khaki, for example, continues sluggish as fashion interest wanes.Carpets, too, leave a

lot to be desired as a slowing housing market could make for a second year of decline.

Floor-covering shipments are expected to be off another 1 to 2 percent in 2002, on top of last

years close to 7-percent slide.Home furnishings markets dont look especially buoyant either. The

past reflects sagging consumer optimism. But other factors here, such as growing imports and a

sluggish housing market, will also tend to put a damper on near-term sales.

No Labor Cost PressuresOn a more upbeat note for all mills, however, is the likelihood

of little or no upward cost tug on the pay front. This past year, labor rates rose by only about

1.5 percent, with only fractionally higher figures projected for 2002 and 2003. Moreover, factoring

in productivity gains, textile unit labor costs have actually been declining.This productivity

factor cant be underestimated as the industry strives to remain at the cutting edge of technology

and become globally competitive in world markets. To ensure this, the industry has invested more

than $2 billion annually in new plants and state-of-the-art equipment from 1987 onward. The figure

reached a peak of almost $3 billion in 1994.In 1999, the most recent year available, industry

capital expenditures were again near the record of just under $3 billion. Upshot: the American

textile industry consistently ranks as one of the most efficient and productive in the world.To

emphasize this last point, the American Textile Manufacturers Institute (ATMI) notes that in 1987,

the average loom produced 12.9 square meters of fabric per hour. Ten years later, the average was

34 square yards a jump of almost 165 percent.Bureau of Labor Statistics output-per-hour figures

tell the same story. They show that this past decades productivity gains for broadwoven fabrics,

yarn and thread, and knitting mills all managed to outpace those made by autos, machinery, paper,

steel and a host of other industries.Indeed, man-made broadwoven fabric and yarn and thread mills

both improved output by more than 50 percent enough to rank these two textile areas 11th and 13th

among 199 industrial categories.Still another measure of productivity progress: A decade ago, the

industry shipped $39.40 worth of product every employee hour. Recent figures show a jump to $54.20

after an inflation adjustment an efficiency gain of 38 percent. The advance was also 30 percent

larger than the average for all manufacturing. These gains have dissipated in recent quarters,

reflecting normal efficiency deadlines during a production downturn. Nevertheless, the fact that

there was no meaningful drop in mill productivity last year has to be regarded as a positive

suggesting a shift back into the gains mode again, if not over this year, then certainly by 2003.

No Fiber Cost Pressures EitherFiber outlays also remain under control. Cotton quotes

have been running close to 30 cents per pound under year-ago levels, marking a 30-year low for this

key natural fiber. More importantly, theres little to suggest that this weak price pattern is about

to end. Both U.S. and global production look to remain quite high at a time when demand has been

doing little more than marking time.On the U.S. production front, some 20 million bales are seen

for the current marketing year. Factor in sluggish demand, and this suggests domestic cotton stocks

will rise 44 percent this year, to 7.7 million bales.Adding to downward price pressure is the

currently strong U.S. dollar. It makes dollar-denominated cotton a lot less attractive to foreign

buyers.The improving quality of cotton has to be regarded as yet another long-term plus for mills

one that should help the industry over the longer pull. In any case, new varieties are being

developed that are higher-yielding, higher-quality, hardier and more pest-resistant.Current

man-made fiber trends also offer some cost encouragement to mills. Quotes have been quite stable

over the past few months, with the governments official man-made producer price index actually

running fractionally under a year ago. And the pattern is pretty much the same where individual

constructions are concerned. At latest report, small year-to-year declines were noted for nylon,

polyester and polyolefins. Looking ahead, many man-mades could continue on the soft side. Aside

from overseas competition and excess capacity, theres the added downward pressure from sagging

crude oil the basic feedstock of most man-mades.How much of a drop A lot depends on when business

picks up and how much oil producers curtail production. But right now, a further 0.5- to 1-percent

slippage in this area is quite possible. Wool, too, isnt likely to cause any headaches. Theres an

ample supply around, with prices of some key grades running only slightly above a year ago. And

cashmere tags are down sharply enough to drop cashmere fabrics by as much as 12 to 15 percent under

last summers levels. Some Further Thoughts on PricesGiven the current supply-demand-cost

situation, its hard to anticipate any meaningful near-term price rebound. Best bet for 2002 is

perhaps a repeat of last years relatively flat pattern at least as far as overall mill product

averages are concerned.

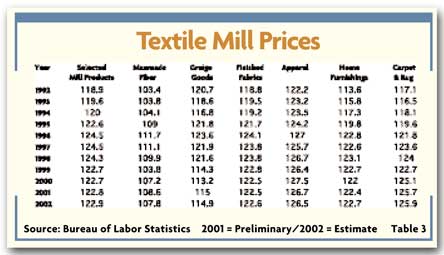

TWs actual price projections for key subsectors of the textile industry are detailed in

Table 3. In virtually all cases, there are no significant advances. Even relatively strong areas

such as denim should continue to have trouble posting higher prices.Beyond 2002, however, some

modest textile price increases are possible as the economy begins to pick up steam, the positive

effects of recent North American trade legislation take hold, and current industry-strengthening

strategies bear fruit. On the latter score, these would have to include additional domestic mill

capacity declines reflecting somewhat reduced capital spending and the impact of plant shutdowns.

All told, industry potential has shrunk 3.5 percent over the past year on top of the previous years

1.5-percent decline. And this trend, which could help bolster prices, looks to continue.In any

event, the longer-run price prognosis is not all that bad. Recent DRI-WEFA projections see average

textile mill product quotes edging up as much as 1 percent annually as we move further into the new

decade.

The Big Imponderable: International TradeBig question marks persist on the foreign

trade front. To be sure, imports may not grow at the pace of recent years, but they should continue

to mean the difference between a healthy and a not-so-healthy industry.If theres any doubt on the

import impact, take a look at the more than doubling of incoming shipments over the past decade.

This increase has far outweighed export gains and made for todays huge textile and apparel trade

deficit. Analysts put most of the blame on the recent Asian currency devaluations. These made for a

huge wave of low-priced textile and apparel imports.ATMI officials note textile imports from Asia

which had shown relatively little growth over a recent 10 years, jumped over 80 percent over the

next four years when Asian currencies dropped in value by an average of 40 percent.Burlington

Industries Chairman, George W. Henderson, concurs, saying that since 1995, the volume of imported

apparel has grown at five times the rate of consumption and that four out of five garments sold in

the United States today are imported.To counter all these developments, ATMI is asking for a longer

carryback period for textile companies with net operating losses; no acceleration of the Uruguay

Round quota phase-out schedule, as sought by many foreign exporters; opening up foreign markets to

U.S. textile exports; stricter enforcement of current trade laws; and strengthening of U.S. efforts

to fight textile transshipments.ATMI also wants to work with supporters in Congress to ensure that

any economic assistance to Pakistan minimizes the impact on U.S. textile and apparel industries;

and enact legislation to clarify that dyeing and finishing of U.S. fabric must be done in the

United States under the Caribbean Basin (CBI) law.Meantime, there continues to be some progress in

the export sphere. Dollar volume totals of outgoing textile and apparel shipments though admittedly

from a very small base have doubled over the past decade.Another positive sign: the shift in

imports away from the Far East and toward North America. Mexico, for example, now sends in three

times the apparel as Asia. The key point: these south-of-the-border imports are mostly made of U.S.

fabrics. Recently passed CBI legislation also has positive implications for domestic mills. Many

now see the Caribbean as at least a partial solution to their current problem. The primary

advantage of CBI sourcing, they add, is speed. In any case, CBI apparel growth should average 10

percent annually over the next few years. After that, an 8-percent growth rate seems likely. But

some of these gains could be at the expense of Mexico.This by no means implies that CBI trade wont

present problems. Some textile executives cite the complicated logistics involved in moving fabric

and apparel from country to country. The paperwork can be overwhelming.Another question mark: what

happens to CBI when trade quotas are eliminated in 2005 Some feel commodity apparel could well go

to Southeast Asia, with the CBI zeroing in on moderate and upper-moderate apparel lines. This, in

turn, suggests the need for domestic mills to develop and sell more novelty fabrics to Caribbean

Basin apparel makers. More New and Improved OfferingsThis emphasis on innovative niche

products, or improved versions of existing ones, could well be the key to survival. Not

surprisingly, virtually every large company has plans for creative introductions to entice

consumers and protect competitive positions.As one mill spokesperson puts it, more people than ever

are going to be interested in newness. Retailers will be more receptive to accept new fabrics, and

manufacturers should have better opportunities to place new products. On a similar note, another

executive said, theres a lot of opportunities if you develop the right fabrics. We always have an

eye open for high-profit niche fabrics that will be difficult for importers to imitate.One example

of the new emphasis is todays growing interest in nanotechnology the changing of the molecular

structure of fibers in a fabric to give it different properties. Some of the developments here

include providing fabrics with wicking, moisture control, and wrinkle-resistant qualities,

providing the soft hand of cotton, but the performance of polyester.In another area, Schaumburg,

Ill.-based Motorola is working on fabrics that can talk to washing machines giving instructions on

how the garment should be washed. Another firm is working on fabrics that allow the expanding of

pants waistlines with the push of a button.At Nano-Tex, Greensboro, N.C., researchers play

basketball everyday in the same socks, engineered with molecular-scaled sponges that absorb the

rancid hydrocarbons responsible for body odor. Another firm hopes to introduce a T-shirt that will

monitor heart-rate, track body temperature and respiration, and even count how many calories a

wearer is burning.Even old standbys such as denim are getting a lot of new product attention. Mills

are developing special denims with unique finishes. They want to avoid basic constructions they

feel can only be sold on the basis of price. There are also a lot more blend denims, especially

with spandex, polyester and polypropylene. Some of these add strength in the fill and wash out more

evenly. Again, its all about specialized markets with one Burlington denim executive observing:

Theres not a million yards of one fabric but a million yards made of 10 fabrics.

The Prognosis Is GoodThe textile and apparel industries are in a state of flux. Changes in

the works will make them almost unrecognizable in a few years. Clearly, these industries will be

smaller, more oriented toward specialty offerings, a lot more efficient, and tuned into the

electronic age. More importantly, all major players will be globally oriented. To assure all this,

advance planning, research and development will be musts. Emphasis will be on items that offer

competitive advantages to end-users.But the prognosis is good. Virtually all analysts now agree

that there will be a viable textile industry five to 10 years down the pike. But the emphasis wont

be on commodity goods, but instead, mainly on high-end goods with a limited but steady market, and

niche products where mills can maintain a competitive advantage.Thats not to say pitfalls wont

continue to exist. One things for sure: once the quota system now in place ends at the beginning of

2005, the industry will be entering unchartered waters.To end on an upbeat note: the textile

industry will survive over the long haul. Indeed, given todays underlying trends and changes, there

should be a lot more plusses to talk about next year when

TW takes its next annual look at the industrys future.

January 2002