Poised For Survival

The US man-made fiber industry adjusts its sights to focus on industrial and home fashions

markets.Recent statistics from the Fiber Economics Bureau (FEB) present interesting and

encouraging patterns of capacity and capacity utilization in the man-made (non-cellulosic) portion

of the fiber industry. This industry has suffered mightily in the recent past, particularly in the

face of increased fiber, fabric and garment imports. The data, however, seem to indicate that,

while these external forces have been substantial, man-made fibers, particularly nylon and olefin,

have weathered this storm with capacities rationalized to levels consistent with a non-apparel

future. The industry looks ready to survive, focusing on submarkets less susceptible to imports

industrial and home fashions while allowing imports to dominate apparel unchallenged. Market

opportunities for US fiber producers will be examined without addressing the minutiae of fiber

price points and relative price advantage. It is axiomatic that the industry must adjust its

capacities to selected markets before price stability and price increase opportunities can replace

the opportunistic pricing confusion of the past five years. This article addresses the

supply/demand balance.All is not rosy; some work remains, particularly with polyesters traditional

and continuing reliance on apparel. Moves have been made, but more are needed. The nylon and olefin

models are instructive, providing continuing operational direction to the remainder of the

industry, and investment perspective to industry participants considering further rationalization

or consolidation in a very mature market.

The SurvivorsIt comes as no surprise that the US man-made fiber industry has seriously

rationalized capacity plans in the recent past. Fiber imports have risen approximately 50 percent

in the past 10 years, having stabilized at this level in 2000. Similarly, fiber exports have risen

approximately 50 percent from 1992 levels, fueled by the economic boom of the 1990s, the North

American Free Trade Agreement (NAFTA) focus toward Canada and Mexico, and some amount of salting

export markets by domestic and international producers. Admittedly, the US fiber export base was,

and still remains, smaller than import opportunities, so comparable percentage gains show a greater

absolute impact on imports than on exports. In the past decade, fiber in the United States has

turned from a net export market to a net import market, a posture unlikely ever to reverse in the

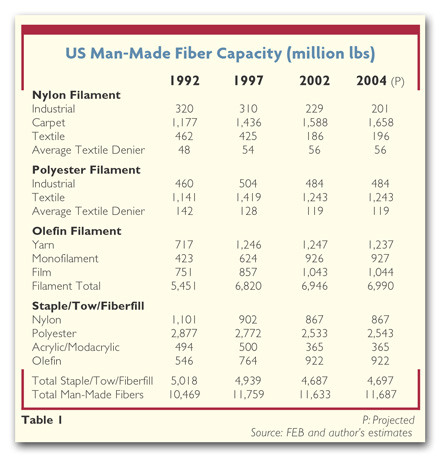

face of actual and planned capacity additions in the developing world.Table 1 details man-made

fiber capacity in the United States from 1992 to 2004. It dramatically demonstrates aggressive

moves by the US fiber industry to reallocate resources toward import-resistant areas of the market,

such as home fashions and industrial, and away from labor-intensive apparel. In the 90s, nylon

producers, facing the combination of polyester incursions in tires and reduced industrial spending

engendered by the late-decade economic slowdown, dropped industrial capacity by one-third and,

facing imported fibers and garments, dropped textile denier capacity by more than half, while

adding 50 percent 500 million pounds to floor covering fiber capacity; all this while operating

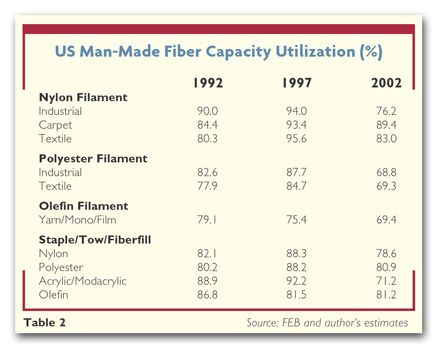

rates for carpet fiber production grew from the low- to the high-80s

(See Table 2). The late-90s reversion of leg fashion from hosiery to bare legs helped

capacity utilization by driving the average textile denier up from the high-40s to the mid-50s.

Honeywells recent purchase of BASFs fiber business and the now-outed secret talks between DuPont

and KoSa for DuPonts nylon properties both look much better in a marketplace supply/demand

analysis. Olefin producers continue to expand filament and staple capacities with the firm belief

that industrial, diaper and carpet end-uses will support this unbridled enthusiasm. Olefins

chemical disaffinity for dyeing long ago inhibited producers spending on development of olefin in

apparel. Rather, the fibers were positioned as inexpensive utilitarian substitutes for some

existing end-uses and attractive alternatives to other materials in new end-uses including:

geotextile fabrics for new markets; fine-denier staple to replace rayon, then polyester, in diaper

coverstock; and relatively inexpensive man-made backing to complement both olefin and competitive

face fibers in carpets. Olefin fibers are not cheap. They are designed to add function to

technology, and producers are rewarded appropriately.As with nylon, market expansion of olefin

fibers has been hindered by the recent US economic malaise. Industrial investment is down, leaving

olefins to survive on low-margin nonwoven materials recent market share battles between

Kimberly-Clark and ProcterandGamble have done much to cap returns for coverstock materials. And the

carpet market has slowed, as the consumer catches up with his industrial counterpart in reducing

spending. If the economy is ever to recover, these two components must start to spend again. Then,

olefin producers, dogged by mid-60s to -70s operating rates, will enjoy the market expansion for

which they have developed fibers.

The ProblemsAcrylic fibers have found several niches that should sustain them, at least in

the short-term. The domestic hosiery industry probably will continue to shrink under import

pressure, but the combination of upholstery, some carpet and acrylics natural affinity for outdoor

use should provide a sufficiently large market to support at least a portion of current capacity.

Recent low operating rates, despite past industry capacity reductions, suggest that further

industry cuts may be in the offing.Unfortunately, polyester fibers are not quite so well-positioned

as are olefins and nylon. Polyester staple was developed as an apparel fiber witness durable press;

and polyester filament fibers were modified into apparel fibers through texturing. Thankfully, the

era of the polyester double knit disappeared into better-styled fashion, but even this fed the

polyester maw in staple blends with cotton.In filament apparel, the decrease in average denier for

polyester in part signals a specialty approach to lightweight apparel 70-denier untextured filament

versus 150-denier for texturing. The recent relatively poor Japanese silk crop, impacted by

reportedly even poorer-quality silk from China, thrust very high-quality fine-denier polyester into

the fashion scene. Demanding quality encouraged many fabric manufacturers to buy domestically; the

logistics/quality/time risk was so great that it offset any price advantages available

offshore.Additionally, filament polyester has found several large markets in home fashions such as

window treatments and nonwovens for the home, and automobile seating structures. To reduce the

fibers reliance on apparel, these must be expanded. Also, while the movement of polyester filament

into tires appears to have slowed, additional efforts must focus on other areas of automotive use

such as hoses, belts, body cloth, tarpaulins and upholstery, to enlarge the position of polyester

filament in specification-driven, import-resistant market areas.Unfortunately, polyester staple is

viewed as an apparel fiber, with significant but not sufficiently large enough to rescue the

industry quantities of fiber going to home fashions and even-smaller-yet quantities going to

industrial fabrications. Until new end-uses are found for polyester, staple and filament alike will

remain under pressure from both domestic and international sources. The likely result is continued

capacity rationalization until a supply/demand balance is reached. Microdeniers, in both staple and

filament, are a partial answer at the upper end of the market, but they will not absorb broader

distribution market losses from continued import pressure.Looking AheadDesign and distribution,

home fashions and industrial these are what the US textile industry does best. The United States is

the largest market in the world. Market control involves concentrating on areas in which there is

competitive advantage. The US textile industry does not have the advantage in labor rates;

labor-sensitive activities, such as garment manufacturing, will continue to move to lower-cost

production areas. It does have the advantage in design and marketing, and knows the market and has

or can develop the skills to service it fully.The US textile industry is a prisoner of downstream

capital and labor offsets in fiber production and must step up and control the future, or it will

be dictated to by a competitor. US producers must develop fibers and encourage rapid development of

fabric and component manufacturing systems unavailable to the competitor that needs six-week

logistics windows. They must target areas less susceptible to imports home fashions, where

logistics advantages and quick response times mean a satisfied consumer. Additionally, US producers

must investigate and actively support new uses for fabrics construction, support, filtration of

both liquid and gaseous materials, ablative materials, heat- and light-sensitive or -resistant

materials, and so on. Then, producers must develop materials, fibers and films to enhance the

natural characteristics brought to the end-use by traditional textile manufacturing techniques.

June 2003