S

ome good news to go along with the bad: Domestic profits, despite earlier fears of a

sharp decline, have remained surprisingly firm. Latest government figures for the first half of

2005 put the industry’s after-tax margin at 3.15 cents per dollar of sales — up a bit from

year-earlier readings. Earnings in dollar terms are up by comparable amounts. Behind the trend are

better cost controls, more savvy management, increased global outsourcing and more concentration on

profitable niche markets.

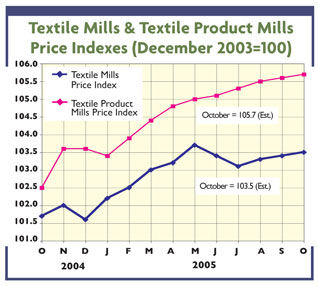

Less bullish, however, are reports of slowly declining domestic mill activity. Just-released

figures show textile mill production running about 3 percent under year-ago levels. Mill sales are

down by about 6 percent.

Not all industry segments seem to be feeling the pinch to the same extent. New numbers for

the basic mill sector suggest a disturbing 12-percent decline from last year. On the other hand,

the more highly fabricated mill product sector has been holding up a lot better, with the numbers

here running fractionally above a year ago.

2006: An Early Look

The same pattern is expected to persist into the new year. Economic forecasting firm Global

Insight sees revenues of basic fibers and fabrics falling 6.5 percent in real or volume terms —

with the drop-off in the mill product area put at a modest 3 percent. In the highly fabricated

product sector, Global Insight sees the possibility of a fractional improvement in profit margins.

While by no stretch of the imagination can all these projections be described as bullish,

they do indicate the domestic textile industry isn’t about to disappear. To be sure, it may be

shrinking, but stronger companies will continue to survive and even prosper in today’s competitive

one-world market — despite the continuing inroads of cheap imports from China and other Far Eastern

nations.

The US-Chinese Pact

The recently inked US-Chinese three-year trade deal should help remove some of the nervousness

and uncertainty that have been plaguing domestic textile and apparel markets over the past year or

so. Not everybody is happy about the agreement — many claim it gives away too much. The National

Council of Textile Organizations, Washington, still views it as an important positive step — noting

that US industry will now know with certainty that China will be unable to flood the market during

the next three years. A spokesman for the group also pointed out that we are retaining our right to

use safeguard quotas should Beijing start flooding the market in categories not covered by the

agreement.

The new bilateral pact limits US import growth in 34 vulnerable clothing and textile

categories. Annual growth of 10 to 15 percent will be allowed during the first year, 2006 — with

the precise advance depending on specific product category. This growth rate should accelerate a

bit to 12.5 to 16 percent in 2007 and 15 to 17 percent in 2008.

Don’t Expect Miracles

Even with this new, comprehensive US-Chinese agreement, it would be unrealistic to expect

anything approaching a return to the quota-restrained import levels of past years. The relatively

high import growth rates just cited would certainly preclude such a bounceback. Equally important

is the feeling that Beijing isn’t about to allow for any major rise in its currency — a move that

might make Chinese goods more expensive. Many now say that even if the yuan did rise appreciably,

it’s doubtful whether major import relief would be forthcoming. Indeed, these doubters feel China’s

cost advantage over the United States would remain fairly impressive even if the yuan were to climb

20 percent against the dollar. Moreover, to the extent China would lose some of its competitive

edge, other low-cost producers in Asia and Latin America would probably pick up most of the slack.

Upshot: While most world-class US firms are likely to survive, their portion of the overall

domestic market seems all but certain to continue falling. Generally speaking, declines will tend

to be the most precipitous in the apparel rather than the textile sector — with perhaps domestic

slippage of 5 percent or more in real or volume terms likely over each of the next three years.

November/December 2005