Spandex Revisited

Changing lifestyles, Third World production will drive spandex growth in coming

decade. About three years ago,

TI explored the world of spandex fibers (See The Textile Industrys Silent Spring, ATI,

June 1998). At that time, we projected spandex use would grow significantly by the beginning of the

new millennium, and industry business models would metamorphose into substantially different

structures.As befalls all who try to prognosticate, TI was right in some conclusions and not right

in others. Specifically, world consumption of spandex materials has not kept pace with

expectations, so the ready availability of comfort stretch garments and materials is less than

anticipated.Unfortunately, the expectations of industry seers led to another miss. Business models

changed dramatically, but the resulting form was almost entirely unexpected. As predicted, the

marketplace has changed dramatically, and the use of spandex continues to rise at significant

rates. However, the competitive environment is totally different from what was expected and

threatens to destabilize spandex marketing and technology. It is time to revisit spandex and try to

refine the picture of this important and changing marketplace. World DemandFrom the

introduction of spandex fibers in the late 1950s, 30 years passed before total world consumption

exceeded 50 million pounds, a level considered large enough to be called a business. By 1985,

DuPont Lycra® controlled 80 percent of spandex distribution. Utility dictated spandex use.

Marketing focused on replacing increasingly scarce and expensive rubber yarns in lingerie fabrics,

girdles, designer full-length womens support hosiery and the cuffs of mens over-the-calf dress

hosiery.Since the mid-1970s, change has rocked textile and apparel markets, as a result of the

impact of Third World labor costs and forces unleashed by the Baby Boomer social revolution. The

former will continue unabated as long as industry searches for better returns from investment and

labor capital. The latter is a revolution in the making, setting new rules of style and comfort

daily. The consumer and the fiber industry believe that additional changes are on the horizon,

changes driven by incorporating elastomeric fibers into new lifestyle clothing.Consumers continue

to alter lifestyles and purchasing patterns. Baby Boomers, the oldest of whom now are approaching

early retirement, driven by egos and self-interest, look to an increasingly casual lifestyle

supplemented by exercise to tone bodies confined to offices in the pursuit of wealth.Spandex usage

rose at an 11-percent compounded growth rate to more than 150 million pounds in 1995, sliding to

7-percent, 211 million pounds, in 2000 in response to such forces as the 1998 Asian flu and the

freedom from panty hose attitude of recent years. Industry seers estimate worldwide spandex demand

will grow between 5 and 10 percent per year for the next decade. TI has built its own projections

on rates slowing from almost 9-percent in 1996 to less than 4 percent for 2001 and 2002, in

response to the current economic slowdown. Sales should recover to almost 6-percent growth by the

end of this decade.Spandex is the prototype niche product. The industry traditionally is divided

into five segments, each of which is further broken down into sub-markets with homogeneous demand

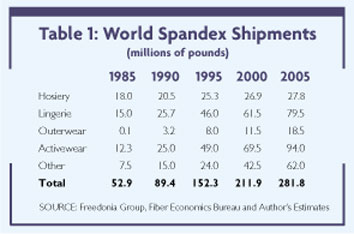

characteristics. Table 1 details recent sales history for spandex and tentatively projects growth

into 2005.

HosieryThere are three markets formal, casual and sport in four segments: mens; womens;

boys; and girls. Womens formal includes full-length nylon hosiery and pantyhose. Casual is cotton,

acrylic or wool ankle and knee-length socks. Sport means nylon staple/acrylic/wool/cotton

sport-specific socks. Mens casual and sport socks are defined the same way as womens, while mens

formal means over-the-calf. Spandex content ranges from barely more than zero in anklet cuffs to

upwards of 15 percent in full-length hosiery and some mens over-the calf items. Spandex in the leg

in full-length womens hosiery usually is bare, but in the panty and cuffs, it is covered with nylon

and/or cotton. Spandex in the body of sport hosiery almost always is covered with the major fiber

in the sock. The covering material is comfortable and compatible with the garment body material, as

well as being a source of dye sites, as urethane-based fibers are notoriously undyeable.According

to estimates, 2000 world usage of spandex in hosiery totaled about 27 million pounds. Of that

total, two-thirds was used in womens hosiery, one-fifth in mens hosiery, with the remainder in

childrens hosiery, split almost evenly between boys and girls. The main component of womens

full-length and panty hose is filament nylon, with approximately 20-percent spandex added for

performance. The industry traditionally categorizes hosiery containing spandex into two groups:

that containing up to 18-percent spandex in sheer hosiery for fit and comfort, and that containing

19-percent and greater for control. In knit fabric construction, the spandex-containing stitch acts

in the horizontal direction, providing stretch and recovery horizontally around the wearers body or

leg. Recent data from The Hosiery Association (THA) exposes annual sheer-hosiery market decreases

in excess of 2 percent for the past 10 years. Increased spandex use in hosiery will come through

increased use in casual and sport socks, where THA data shows a 7+ percent 10-year annual increase,

largely the result of the casual Friday phenomenon.Market sources estimate less than 25 percent of

casual and sport hosiery currently contains spandex. Because the fiber has been available for more

than 40 years, it is unlikely that there will be a rapid conversion of the remainder. Spandex adds

cost, and because many socks are purchased for utility, fashion influence is limited. Spandex will

continue to penetrate socks at a 2- to 3-percent annual rate. InnerwearInnerwear, or lingerie

for women and underwear for men, encompasses myriad products made from virtually every fiber

converted into fabric by virtually every known method. According to current estimates, innerwear in

2000 consumed approximately 61+ million pounds of spandex, with 40 percent used in brassieres, 10

percent in shapewear, 20+ percent in panties, 10+ percent in sleepwear, 10 percent in womens

daywear, a relatively minor amount in robes and loungewear and the remaining 10 percent spread

across a variety of womens garments, plus waistband and leg cuff materials in mens briefs and boxer

shorts.Industry forecasts predict 7-percent annual penetration growth in bras and shapewear. The

modern consumer wants to look and feel better, which means a combination of activities and clothes

designed and constructed to enhance a trimmer figure. Exercise demands for sport-specific

body-support innerwear will provide the impetus for most of the growth expected in the market area.

Sport participants and wannabes want shapewear to hide imperfections even the most rigorous

exercise program cannot repair. While the modern shapewear woman rejects the control garments her

mother wore, she recognizes derriere, stomach and bust lifters and waist thinners as serious pieces

of apparel.Generally, lingerie is made from cotton and/or filament nylon or polyester. When spandex

is present, it usually is wrapped with the primary fiber. Overall spandex content ranges from 2 to

3 percent for hem, lace and cuff applications; up to 20 to 25 percent for body-control garments;

and approaching 50 percent for girdles and waist-cinch garments. OuterwearOuterwear means only

that it is not innerwear. Spandex is used in constructions targeted at dress suiting, shirting, and

dress and active sport clothing for men and women. The spandex proportion of the total fabric is 2

to 5 percent, just enough to provide fit and comfort. Bare spandex is used in circular knits by

platting an end of spandex with an end of the body yarn through the same needle. Wrapping is the

covering system of choice, but technology improvements are expected to help core spinning replace

wrapping in several years. Wrapped spandex yarns, depending upon end-use, usually are covered with

cotton yarns or nylon or polyester continuous-filament fibers and are knitted or woven. In Europe,

work has focused on wool as the covering fiber, but logic suggests that cotton, aimed at the more

casual U.S. market, offers more opportunities.Woven outerwear comfort garments containing spandex

are largely European phenomena. Demands for high productivity in the U.S. textile/ apparel complex

to compete with international fabric suppliers and imported garments have relegated woven comfort

outerwear to a minor role. Textured polyester filling stretch falls short of the classical

definition of comfort, and, in light of developments in spandex-containing fabrics, textured yarns

should be viewed as fair-to-poor attempts to expand a boring bottom-weight market.Spandex growth in

outerwear is heavily based upon penetration by fiber blends targeted at dress suiting, shirting,

and dress and active sport clothing. Dress-down Fridays provide the impetus for woven, fitted but

comfortable dress-up/dress-down apparel. The spandex proportion of the total fabric is 2 to 5

percent, sufficient to provide fit and comfort, but not enough to be called control or power. The

almost 50-percent growth projected for spandex in outerwear from 11.5 million pounds in 2000 to

almost 19 million pounds in 2005 is due almost entirely to increased interest in woven-filling

stretch comfort fabrics aimed first at sportswear and later at dress

garments. ActivewearAccording to DuPont, the top U.S. participation sports are exercise

walking (73 million people), swimming (60 million), biking (53 million) and exercise with equipment

(48 million). Apparel for these groups forms the backbone of the activewear category a major area

for spandex but one that will experience slowing growth, as the smaller Generation X fails to buy

as many activewear garments as does/did the predecessor Boomer generation.Activewear includes

sweatpants, sweatshirts, jogging suits, T-shirts, elastic-waist shorts, warm-up jackets, leotards,

swimwear, skiwear, biking garments, etc. It includes garments with an athletic heritage redesigned

to be equally at home in the supermarket as on the tennis court. Activewear implies power, so

spandex content and fabric manufacturing technique are geared to the amount of control desired from

the garment. Most activewear spandex is run-wrapped and most activewear is knitted, but woven

materials are finding their way into the category.

In 2000, world usage of spandex in activewear approximated 70 million pounds. Best estimates

indicate that approximately 23 million pounds is used in swimwear, about 10 million pounds in

full-length sport-specific tights/leotards, with another 12 million pounds for the cuffs, hems and

some bodies of sweat apparel. About 27 million pounds is used in T-shirts, warm-up jackets,

dancewear, leotards, biking garments, etc.Swimwear fabrics contain a higher percentage of spandex

than all other categories except power/control garments an average of 15 to 17 percent with some

extra-control items containing up to 31 to 35 percent. Under most circumstances, nylon, with its

affinity for high colors, is the companion fiber. Swimwear demands spandex resistance to chlorine.

Fibers lacking this property are precluded from long-term competition in the market, and

improvement in this characteristic is high on every serious producers list. Sport-specific

tights/leotards have bright colors in every form of print and geometric design. Natural heirs to

hosiery and dance histories, this category is not expected to grow significantly in the next

decade. Spandexs proportion in a tight/leotard fabric is approximately the same as in swimwear,

with nylon the other component for strength and color. Major quantities of sweat apparel were

produced in the early 1990s, and the market continues to struggle with overcapacity. After crashing

and burning in 1998-99, the baggy sweat appears to have been replaced by a slimmer, trimmer

silhouette. No growth is seen in sweats.It is virtually impossible to parse the approximately 27

million pounds of spandex in T-shirts, elastic-waist shorts, warm-up jackets, dancewear, leotards,

skiwear, biking garments, etc. into specific categories. These activewear producers are

geographically and stylistically diverse, supplying small amounts of special apparel to smaller

retailers that service specific sport or market areas. Other ApplicationsOther applications

for spandex, totaling 42+ million pounds in 2000 and projected to grow to 62 million pounds in

2005, include such end-uses as waist and leg cuff tapes in disposable diapers and clean-room and

hospital apparel, components of shoe linings, Ace bandages and braces, fitted bed-sheet edges,

slipcover edges and high-performance protective clothing including space suits. Spandex is expected

to increasingly penetrate markets such as disposable hospital and clean-room apparel, shoe linings

and protective clothing in the coming decade, to provide the almost 50-percent increase projected.

One caveat: spandex use in disposable diapers might be replaced within five years by meltblown

elastomerics and/or elastomeric films, particularly where returns on capital and product

differentiation strategies drive replacement of expensive yarn processing with efficient film-type

materials. ExportGenerally, export should not be treated as a separate market area, but the

peculiarities of spandex growth make a separate discussion appropriate. Until the 1980s, DuPont

dominated spandex distribution and was able to sell most production in U.S. markets. As

international economies increasingly industrialized, spandex-containing garments became attractive

and affordable. DuPont seeded these markets with fibers from its plant in Waynesboro, Va., and

later built fiber plants around the world nine today, with more on the drawing board. In DuPonts

mind, export was a temporary handmaiden of expansion; the strategy was expansion, not export. The

distinction is important, particularly in light of the current market. DuPont controlled product

distribution and, more importantly, controlled the use of cash in international expansion.

In contrast, todays international market is a hash, driven to pure price competition by

developing-nation, often state-sponsored export strategies designed to employ a maximum number of

people and amass baskets of hard currencies. A building boom has made Asia a huge exporter of

spandex fibers. The original logic behind the boom, in Korea particularly, has evaporated, and it

appears that these bloated international firms are willing to sell at any price, hopeful of

covering variable cost. A U.S. or European producer cannot compete with this Asian tiger.Export

will continue to be important through 2005. However,

TI expects the positive balance export has brought to the United States will evaporate as

DuPont ceases Waynesboro seeding, developing economies continue to pour product into the United

States, and continuing international price pressure forces U.S. producers out of the world market.

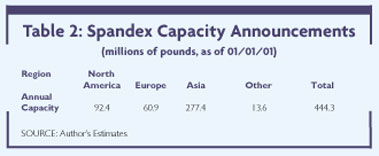

CompetitionTable 2 lists current reported spandex capacities by major world region. The data

comes from the press and U.S. private and government sources. Because timing and capacities from

these sources tend toward significant overstatement,

TI and other industry observers estimate year-2000 effective world capacity at 397.0

million pounds. Asian reports, particularly, are subject to harsh review.

Expansions announced for the next two years in Asia only serve to exacerbate the

discrepancies.

TI assumes that wiser heads will prevail, see overcapacity as the root cause of reduced

margins and postpone/cancel some announced intentions. Competition in the United States is not

among the three domestic producers. It is between the investment demands of industrialized

economies and those of cash-hungry, surplus-labor-driven developing economies of Asia. DuPont alone

continues to support a serious brand strategy that has been successful in maintaining price and

stability. But even Dupont is folding. Recent announcements from company headquarters highlight

agreements to build several thousand tons of unbranded spandex capacity in Asia. This strategy

ensures the success of the Lycra brand and turns the competition into DuPonts partner with an

investment in its future. PricingLycra prices changed very little between 1995 and 1998, but

they did respond to domestic and import pressures in 1999 with a denier-selective decrease

approximating 20 percent, particularly in finer deniers. Prices for domestic unbranded spandex have

maintained an almost constant 15-percent discount against Lycra.New spandex capacity in Asia was

built largely around 40- and 70-denier yarns, the backbones of the areas circular (single) knit

industry. As the T-shirt market tanked in 1997/98, Asian producers looked to the United States as

an obvious and attractive outlet for excess capacity. The effort began in the mid-1990s during the

Asian flu crisis, but it has reached fever pitch in the last 18 months. The result is seen in

prices for imported spandex on tubes, which dropped dramatically in 1999. Seventy-denier reached

the $7.00 level by year end, down from $10.00 a year earlier, and 40-denier reached $7.50.

Seventy-denier import pricing is 13 percent below unbranded domestic supplies and 26+ percent below

Lycra. Forty-denier is 32 percent below unbranded domestic offerings and 52 percent below Lycra. An

October 2000 item in the Korea Herald reported domestic (Korean) spandex prices were averaging

$4.53 per pound, close to manufacturing cost, down from $7.03 a year earlier. ConclusionsWhile

conclusions are sprinkled throughout this piece,

TI wishes to emphasize the more important ones.Sales Volumes. World demand for fabrics

with elastic properties will continue to grow. Growth largely will be driven by increases in

comfort vis-is power garments. As Baby Boomers and Generation Xers approach sedentary lifestyles,

they will search for comfort over power.Imports. There is nothing to indicate that imports will

decrease in the immediate future. It is obvious that several countries in Southeast Asia have

embarked on a building binge apparently aimed at controlling the world fiber/fabric/garment

industries. The gamble is so large, so politically sensitive and so demanding of cash infusions

that turning off the international spigot is virtually impossible. Brands. DuPonts continued

perseverance in actively supporting the Lycra brand is admirable. That, and DuPonts historical

technological lead, have proven to be effective strategies in fending off domestic price pressure.

The jury is out, however, on the brands ability to continue to maintain price differentials in the

face of increasing international pressure. It is conceivable that DuPont will further join the

competition by servicing some/all U.S. accounts with product imported from partner/ licensee

companies in Asia.Pricing. Imports and overcapacity hold the keys to spandex pricing and to brand

maintenance. The bottom line likely will surface this year, and we should discover the real costs

of spandex manufacturing in Asia. Until then, it is anybodys guess when some of the more active

exporters will drop out. Until such time, spandex pricing likely will be weak.Production

Capacities. The market must wrestle with the capacities shown in Table 2. Compared to polyesters

mature position on the product life-cycle curve, spandex still is a growth-phase material. DuPonts

brand activities and chlorine resistance are differentiating strategies aimed at extending the

growth phase and minimizing the evolution of competition and pricing strategies apparent in

life-cycle maturity. Unfortunately, spandex price strategies, driven by capacity investment needs,

have moved ahead of development efforts and might inhibit fabric innovation and expansion. The only

logic bringing stability to pricing is shrinking the list as planned and actual capacity proves

unprofitable. Market Expansion. The five market areas will take significantly different paths to

expansion. All are forecast to grow, but for different reasons: hosiery, virtually stagnant, will

grow marginally through continued spandex penetration of ankle hosiery, while sales to innerwear

will expand as comfort fabrics displace traditional rigid versions. Activewear relies on consumer

health responses with increased active sportswear and wannabe participation. In our view, only

outerwear nears a revolutionary transformation. Because minor amounts of spandex can effect major

changes in fabric performance, the recent somewhat lower fiber prices likely will engender mill

interest in spandex-containing suit, dress and sportswear constructions. Unfortunately, however,

U.S. fabric mills may find themselves at a technological disadvantage with European counterparts

because many lack the hardware needed to produce the special-width fabrics for finishing into

standard- and wider-width fabrics demanded by cut-and-sew operators. U.S. mill survivors will have

to invest dollars they think they dont have. Editors note: John E. Luke is owner of Five

Twenty Six Associates Inc., Bryn Mawr, Pa., a consulting firm specializing in strategic marketing

and operations facing textile fiber and fabric manufacturers. He is also a professor of textile

marketing at Philadelphia University, Philadelphia.

May 2001