![]() ZÜRICH, Switzerland — June 8, 2026 — The global textile industry appears to be turning a corner, but this is more likely a fragile and possibly temporary improvement than the start of a durable recovery. According to the 38th ITMF Global Textile Industry Survey, conducted worldwide during the second half of May 2026, business sentiment, order intake, order backlogs and capacity utilization all improved versus March — yet every indicator remains weak by historical standards, and rising costs cast doubt on how long the upturn can last.

ZÜRICH, Switzerland — June 8, 2026 — The global textile industry appears to be turning a corner, but this is more likely a fragile and possibly temporary improvement than the start of a durable recovery. According to the 38th ITMF Global Textile Industry Survey, conducted worldwide during the second half of May 2026, business sentiment, order intake, order backlogs and capacity utilization all improved versus March — yet every indicator remains weak by historical standards, and rising costs cast doubt on how long the upturn can last.

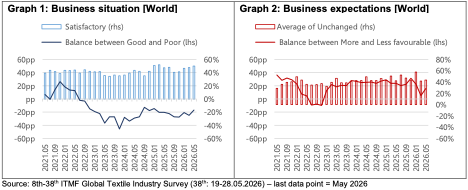

The new survey shows a business situation balance rising to −17 percentage points (pp) from −25pp in March. Business expectations climbed to +16pp (from +5pp), order intake to −9pp (from −25pp), backlogs to 2.5 months and capacity utilization to 74%. Order cancellations stayed contained and inventories lean low. The direction is encouraging, but the levels rest on a thin and fragile cushion.

The upturn was geographically uneven. Africa led on business situation, order intake, backlog and expectations, alongside gains in Europe and North & Central America. The Asian production hubs lagged, with East Asia weakest on both current conditions and the six-month outlook. Along the value chain, segments closest to the end-consumer slightly fared best, while capital-goods and upstream segments trailed.

The upturn was geographically uneven. Africa led on business situation, order intake, backlog and expectations, alongside gains in Europe and North & Central America. The Asian production hubs lagged, with East Asia weakest on both current conditions and the six-month outlook. Along the value chain, segments closest to the end-consumer slightly fared best, while capital-goods and upstream segments trailed.

Cost and demand pressures persist: weak demand remains the major concern for 53% of participating textile manufacturers, followed by raw-material prices (52%) and energy prices and geopolitics (42% each).

![]() The survey links rising costs to the war in Iran, which has pushed crude oil to around USD 100 and lifted gasoline prices by roughly 50% since March, feeding inflation and squeezing margins. Whether the May reading holds will depend largely on energy prices and the resolution of ongoing conflicts.

The survey links rising costs to the war in Iran, which has pushed crude oil to around USD 100 and lifted gasoline prices by roughly 50% since March, feeding inflation and squeezing margins. Whether the May reading holds will depend largely on energy prices and the resolution of ongoing conflicts.

For more information, please see www.itmf.org or contact secretariat@itmf.org.

Posted: June 9, 2026

Source: International Textile Manufacturers Federation (ITMF)