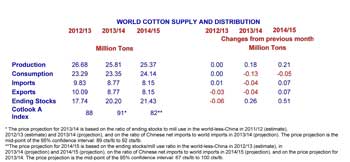

WASHINGTON — July 1, 2014 — Higher ending stocks outside China and lower imports into China will put downward pressure on international prices in 2014/15. Additionally, world production is likely to exceed consumption in 2014/15, though by a lesser amount than in the past four seasons. As a result, world ending stocks are expected to rise by 6% to 21.4 million tons and the stock-to-use ratio would be 89%, or in other words there would be enough cotton stocks to cover consumption for nearly 11 months. This would be the fifth consecutive season of increase in ending stocks, after a 27% fall in 2009/10. China is estimated to hold nearly 60% of the world’s stocks, most of which is held in its government reserve. At the end of June, the Secretariat estimates that the Chinese government will still hold 11.7 million tons. While consumption in China is forecast to grow during next season, a strong preference exists for high quality cotton, so it is unlikely that the government will be able to quickly draw down its reserve without offering significant discounts. At the end of 2013/14, China is forecast to hold 11.5 million tons, an increase of 19% from 2012/13, and these stocks are likely to further expand in 2014/15. Additionally, ending stocks outside China are also expected to rise by 7%, to 8.7 million tons at the end of this season and are projected to reach 9.7 million tons at the end of 2014/15.

In 2014/15, world production is forecast to drop by 2% to 25.3 million tons due to reduced planting in China, where cotton production may reach only 6 million tons. Production in the rest of the world is expected to increase by 1% to 19.3 million tons. In 2013/14, production in India is estimated at a record 6.5 million tons due to higher yields and better prices, which encouraged farmers to plant more cotton in 2014/15. Assuming yield is similar to the 3-year average, Indian cotton production is projected to reach 6.3 million tons in 2014/15, but this result is highly dependent on the timing of monsoon rains. The Southwest region of the United States has received much needed rain, which could help reduce the abandonment rate and result in a higher harvested area than last season. In 2014/15, production in the United States is expected to grow by 14% to 3.2 million tons.

In 2013/14, world consumption grew by less than 1% to 23.4 million tons, but a rise of 3%, to 24.1 million tons is anticipated in 2014/15. The high price of domestic cotton in China, restrictions on imports, difficulties with financing and weak demand for cotton yarn have caused many mills in China to further reduce operations this past season. However, with the ending of China’s reserve policy, many mills are anticipating lower prices later this year, as already reflected in futures markets. Consumption in China should improve slightly and reach 7.9 million tons 2014/15. India experienced strong consumption growth in 2013/14, increasing by 5% to 5.1 million tons. In 2014/15, consumption is projected to grow by an additional 6% to 5.4 million tons.

World trade is projected to decline by 8% to 8.1 million tons, as a result of a reduction in China’s imports from 3 million to 2.2 million tons next season. Imports in the rest of the world are forecast to rise by 3% and reach 5.9 million tons. Imports into Southeast Asia have grown in line with the expansion of consumption in the region, since little cotton is grown there. In 2014/15, the Secretariat expects imports by Bangladesh to increase by 2%, to nearly 900,000 tons, and those of Vietnam to rise by 9%, to nearly 700,000 tons.

Please click chart to view larger